Belarus is still recovering from the financial and banking meltdown of 2014-2016. Meanwhile, the government in neighboring Russia is seeking ways to reduce the role of the USD in state finances, due to sanctions being imposed by the US and European Union. “Belarus has the highest share of FX deposits among Central and Eastern European (CEE) countries at around 70 per cent, and one of the highest shares of FX lending at close to 60 per cent,” the International Monetary Fund (IMF) said in a paper published in December 2018. “Past crises, hyperinflation and strong depreciation episodes have undermined trust in the local currency, therefore triggering economic agents to switch their savings and borrowings to foreign currency,” IMF added.

Indeed, in only the past decade, Belarus has endured three financial crises, the most severe of which happened in 2011, when the domestic currency lost two thirds of its value and inflation reached 108.7 per cent. In the following year, 2012, inflation in the country remained above 65 per cent.

“Belarus is the champion of cumulated depreciation of its national currency throughout the whole post-Soviet space,” Alexander Chubrik, head of the Minsk-based IPM Research Centre economic policy think tank, told the CE Financial Observer.

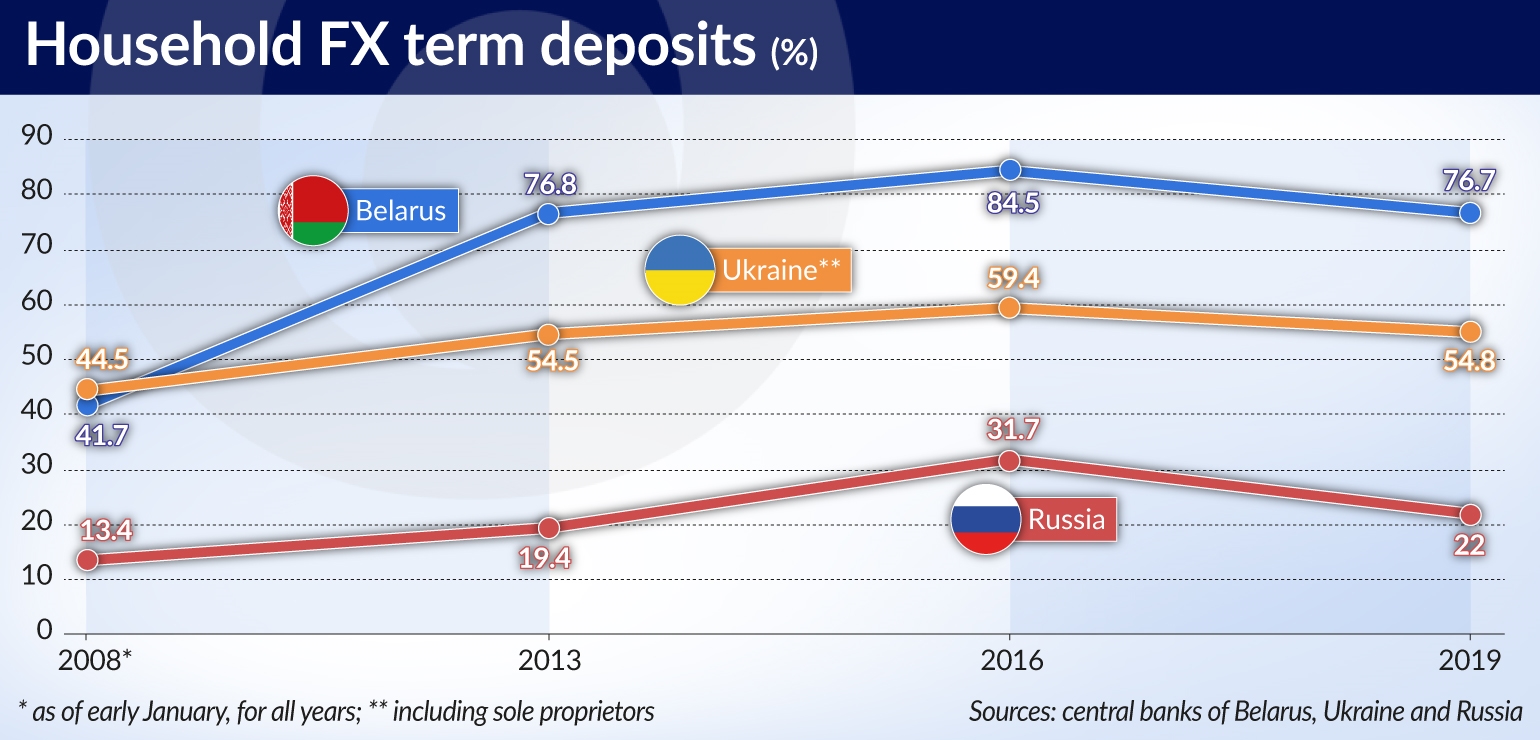

According to the IMF, trade and financial linkages with the rest of the world would predict a benchmark dollarization level of about 20 per cent. The share of household FX deposits has been decreasing from a peak of over 80 per cent in 2015, but was still around 77 per cent as of early January 2019. For comparison, this level stood at only 35 per cent in 2006, before the global financial crisis.

Loan dollarization is also high for corporations, currently at 65 per cent (vs. 40 per cent in 2006). At the same time, however, FX lending to households has fallen as a result of a ban imposed by the Belarusian authorities in 2009 on household FX borrowing.

According to estimates by the Belarus’ central bank (NBB), a 1 per cent decrease in the BYN/USD exchange rate would entail a loss for enterprises of BYN230m (around USD110m), resulting from the revaluation of the FX debts owed to Belarusian banks. The loss to the state budget resulting from a revaluation of the national external debt would be around BYN330m.

“The overall impact on the country that would result from dollarization is a loss of around 2-3 per cent of GDP annually”, said the first deputy governor of the NBB, Sergei Kaletchits, in the mid-2018.

No alternatives

“There are no alternatives to banking deposits in Belarus at the moment,” Mr. Chubrik said. “The market for private funds is still embryonic, and long-term instruments are not sufficiently developed because of lingering mistrust in the stability of macroeconomic policies. So the only option left is to save up in foreign currency — this has been the most reliable way of protecting one’s savings. Moreover, bank investments are insured in full,” he added.

Belarus has recently undertaken measures to mitigate the high level of dollarization. Macroeconomic stability and lower levels of inflation in the last few years have contributed to a higher rate of confidence in the local currency. Appropriate prudential measures have also been introduced, according to the IMF.

Specifically, Minsk’s fiscal policy has remained relatively prudent in recent years. The government deficit has stayed below 3 per cent. Monetary policy has improved materially through a more rules-based monetary policy framework that is less subservient to fiscal or state-owned enterprises and has price stability as its objective. A monetary aggregate targeting framework was also introduced in early 2015, with a focus on gradually transitioning towards inflation targeting.

As a result of these and other measures, the level of household FX deposits declined from 84.5 per cent in January 2016 to 76.7 per cent in January 2019.

“The fact that dollarization has slightly decreased for the third year in a row is fully a result of the efforts of the national bank in its current makeup,” Mr. Chubrik said and added “I would have given [the regulator’s governor Pavel Kallaur] the title of Governor of the Year in 2015 — he was able to prevent the collapse of the financial market whilst working with reserves that were less than the state’s current liabilities at the time. Now even bribes are offered in BYN — something previously unheard of in Belarus.”

However, the IMF believes that some key components are missing. In particular, domestic capital markets are shallow and in their current state act as a brake on de-dollarization efforts, according to IMF experts. “The authorities are also planning some longer-than-one-year BYN denominated issuances for 2019. These efforts will need to be stepped up for there to be a proper benchmark yield curve. In parallel, efforts are needed to create institutional demand for longer term bonds, which is currently lacking,” the IMF wrote in its paper. “An overarching and publicly communicated national strategy to de-dollarize the economy is a missing piece of the puzzle,” the IMF added.

Meanwhile, Ukraine started this year with a level of household FX deposits of around 55 per cent, a slight decline compared to 2015-2017, when deposits stood at around 60 per cent. During the previous decade, extreme effects on the deposit market were felt only in 2009, when FX deposits reached almost 60 per cent as a result of the negative impact of the global financial crisis on the country’s economy.

Materialized FX risks

Ukraine’s domestic currency, the UAH, depreciated from around UAH8 per USD1 in early 2014 to about UAH15 in December of the same year, while in 2016-2018, the exchange rate stood at UAH25-28 per USD1. “Despite seasonal volatility, the UAH exchange rate has remained stable since 2016. However, we cannot speak of any serious confidence in the national currency — memories of past depreciations are too fresh,” Mykhaylo Demkiv, a financial analyst at Kyiv-based consultancy Investment Capital Ukraine (ICU) told the Central European Financial Observer. At the same time, UAH savings are boosted by the higher interest rates on accounts in the national currency compared to FX savings.

“Foreign currency risks materialized fully during the past crises, which were marked by episodes of substantial hryvnia depreciation,” Ukraine’s central bank, NBU said in its December financial stability report. “Banks were hit by deposit outflows. Depreciation made it harder for households and businesses to service loans, pushing the NPL ratio up.”

For this reason, Ukraine’s parliament has adopted legislative restrictions on foreign currency lending to households. However, there are no legal limits on foreign currency lending to the corporate sector, according to the regulator. “At the same time,” Mr. Demkiv added “the country’s banks are reluctant to lend foreign currency to companies that do not have sufficient FX earnings to service their loans.”

FX loans dilemma

According to the NBU, the dollarization rate of loans differs dramatically across different groups of Ukrainian banks. Banks with Russian state capital, at which foreign currency loans comprise up to 90 per cent of loan portfolios, lead the way in terms of dollarization. Most of these are legacy loans. “The loan portfolio of these banks is not currently growing; foreign currency lending has been limited in recent years,” the NBU added.

At the same time, a number of banks with western capital have a share of foreign currency loans below 30 per cent, even though they can tap relatively cheap foreign currency funding from their parent banks. The significant losses those banks incurred during past crises, because of portfolio dollarization, taught them a lesson, motivating to cut their foreign currency loan exposures by 15–20 percentage points, the NBU believes. However, some banks at which foreign currency loans hold more than a 50 per cent share of all loans, continue to lend intensively in foreign currency.

The NBU is convinced that the high level of portfolio dollarization at banks exposes them to systemic risk. If banks fail to take sufficient action to reduce balance sheet dollarization, the regulator may apply additional risk weights to foreign currency assets and tighten the requirements for assessing the credit risk of foreign currency loans. “These measures are designed to reduce foreign currency risks for banks and their clients,” the central bank warned in its report.

To demote the USD role

The financial behavior of the Russian population differs dramatically from both Ukraine and, especially, Belarus. Notwithstanding western sanctions that were triggered after Moscow’s annexation of Crimea and the Donbas war, as well as sharp depreciations of the domestic currency in recent years, the level of deposit dollarization stood at only 22 per cent as of early 2019.

Even at the peak of the current crisis in early 2016, this figure was only slightly above 30 per cent. At the same time, the RUB depreciated from RUB33 per USD1 in January 2014 to RUB73 per USD1 in December 2015.

“The authorities can feel comfortable with the levels of FX deposits in Russia, which are in fact comparable to some markets in Central Europe that have had far more stable currencies over the past five years compared to the Russian ruble and other CIS currencies,” argues Martin Belchev, Central and Eastern Europe analyst at Washington-headquartered consultancy DuckerFrontier.

“It is in fact remarkable that, given the geopolitical pressures and relatively low consumer confidence, we have not seen sharp rises in FX deposits. However, part of the explanation may lie in individuals’ preference to keep hard foreign currency in cash,” Mr. Belchev told the Central European Financial Observer.

Meanwhile, the Russian cabinet is set to demote the USD role in the state’s finances, due to existing sanctions by Washington, as well as the looming threat of new ones. Last year, the government said it is working on reducing the Russian economy dependence on the greenback, “including through stimulation and the creation of mechanisms to shift foreign-trade settlements to national currencies”.

One of the most ardent promoters of de-dollarization in Russia is Andrei Kostin, CEO of a state-owned VTB Bank. In 2018, he announced his own plan for de-dollarization, which would take about five years and involve increased usage of local currencies in international trade (the EUR, CNY and RUB); re-registering major companies in Russia; and using the local financial infrastructure for Eurobond issues, according to Bloomberg.

The Russian government will surely continue to encourage the further de-dollarization of the private and public sectors, and might even offer some fiscal incentives to companies that conduct their business in currencies other than the USD, Mr. Belchev believes. “However, it is also aware that large businesses, especially in the hydrocarbon sector, depend on the USD, and so it is unlikely that they will push for more active measures in the private sector,” he added.

He said that putting actual pressure on companies to de-dollarize their FX debt, however, is unlikely. “The USD is preferred among investors for doing business or issuing corporate debt, and additional measures to diversify corporate FX debt might be misread by international markets,” Mr. Belchev stressed.

Growing role of CNY

According to official data supplied by Russia’s central bank, the regulator halved its USD assets to USD100bn (22 per cent of total) in the Q2’18, replacing it with EUR, JPY and CNY. The biggest surprise for analysts was a massive purchase of CNY, which went up by the equivalent of USD44bn.

“At first glance, the spike to 15 per cent may seem like a catch up with the growing role of China in the Russian external trade turnover, which has been growing steadily over the last years and went up to 15 per cent in 2017-2018,” Dmitry Dongin at ING Bank wrote in his research note in January.

“However, it is also known that China-Russia trade is 70-90 per cent USD-denominated due to the product mix, and the role of the CNY in Russia’s trade turnover is equivalent to around USD10bn per year, which corresponds to only 2 per cent of Russia’s external trade. By that metric, the USD67bn worth of CNY in the Central Bank of Russia reserves appear massive and may reflect Russia’s political preference for a more prominent role to be taken by China as Russia’s trade and investment partner in the future,” he added.

Mr. Belchev believes that Russia’s purchase of the CNY worth USD44bn should be seen as an attempt to foster closer economic and political ties with China. “Additionally, the government has been quite vocal in its support for conducting trade in currencies other than the dollar, but the low trade turnover rate suggests that the economic benefit of purchasing the yuan makes less sense economically than geopolitically,” he said.

Meanwhile, the Russian leadership’s moods indicate that Moscow’s stance towards the USD and the Washington-led sanctions is part of a long-term strategy. “They [the US] will never lift their sanctions against Russia because their entire policy over the past hundred years has been built on the endless application of sanctions against our country, whatever it was called; the Soviet Union or the Russian Federation,” Russia’s Prime Minister Dmitry Medvedev said on March 29th.