At the beginning of 2019 new tax burdens entered into force in Romania, introduced through a special legislation at the end of the previous year. They were necessary due to the growing imbalance in the Romanian public finance sector in recent years.

In 2018, the deficit of that sector — according to the ESA 2010 methodology — amounted to 3.3 per cent of GDP. This is the highest deficit in the European Union, exceeding the EU budgetary discipline criterion under the excessive deficit procedure (a maximum of 3 per cent of GDP). The new tax burdens covered the banking, energy and telecommunications sectors, as well as the gambling industry.

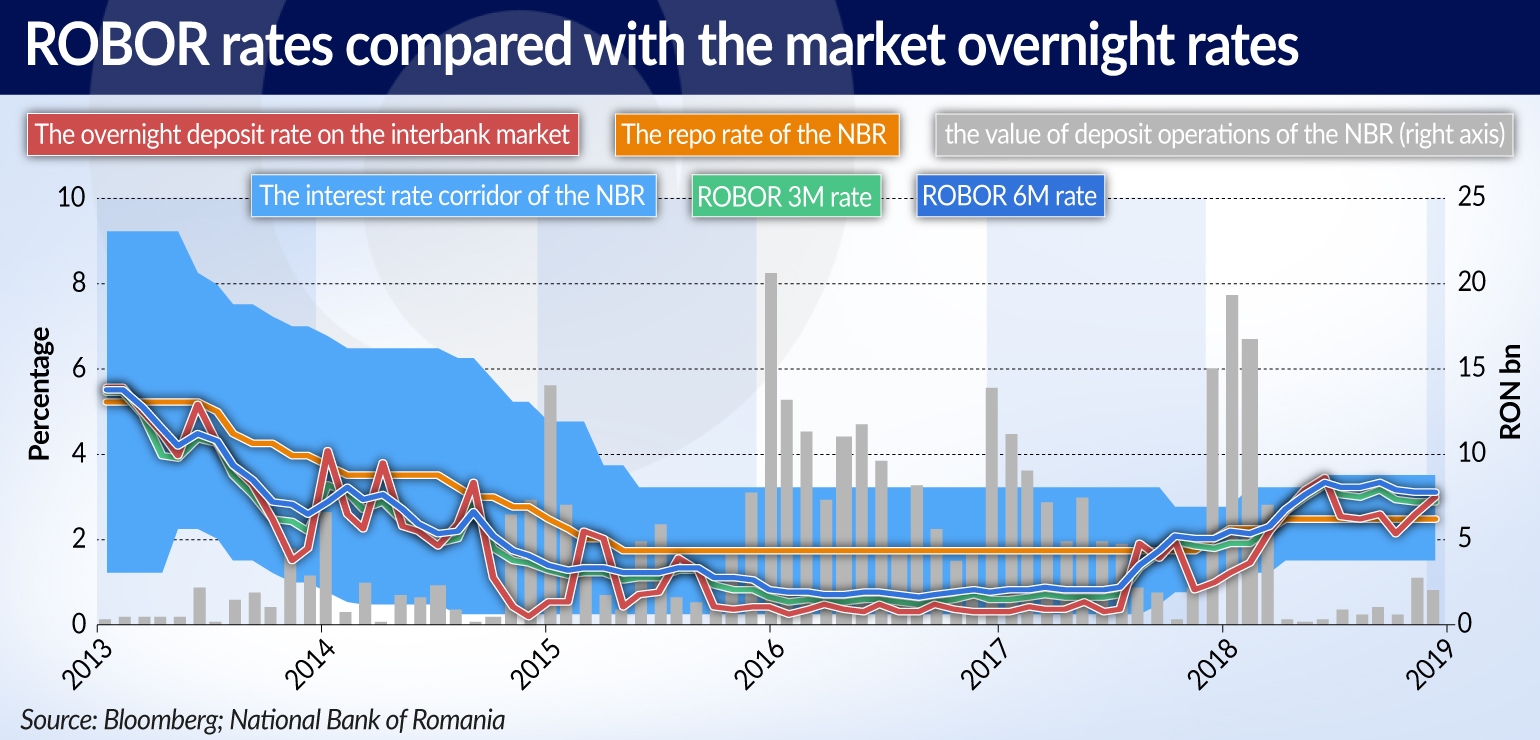

The higher the interest rates, the bigger the tax

All the industry-specific taxes have caused controversy. However, these controversies were particularly intense in relation to the bank tax. This was due to the fact that its rates depend on the interest rates on the country’s interbank market. According to the assessment expressed by the Romanian central bank (BNR) in its summary of the discussions at the February decision-making meeting, this would mean that the “tax is linked to the monetary policy stance”.

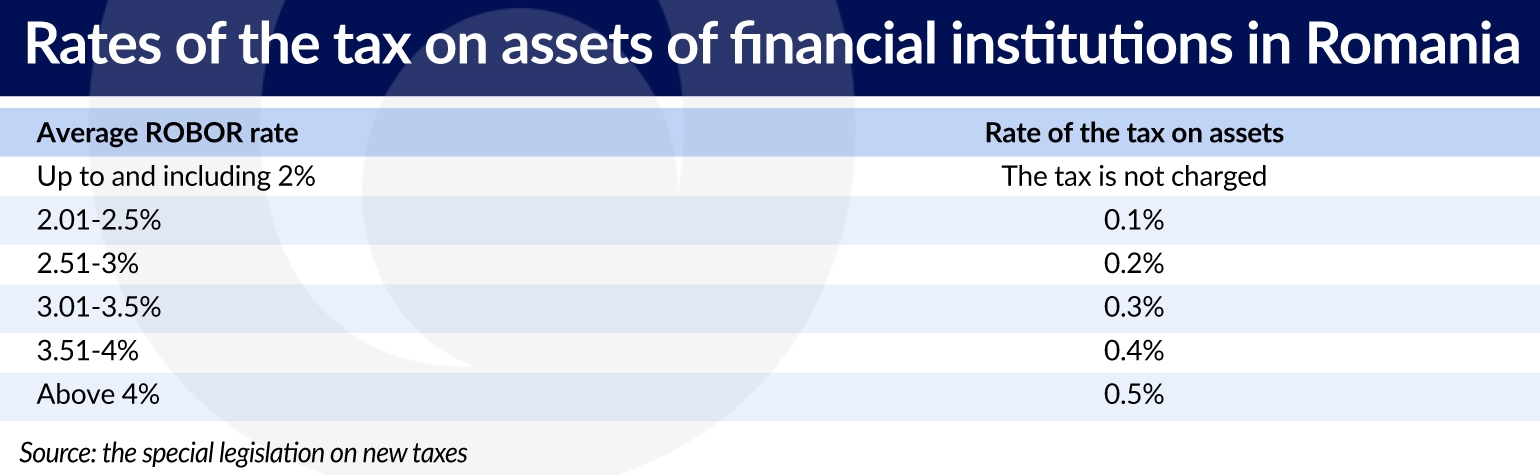

If the rates on the Romanian interbank market — and, specifically, the average quarterly level of the ROBOR (the equivalent of WIBOR) interest rates for loans with 3-month and 6-month maturities — are sufficiently low (2 per cent at the most), then the tax is not charged at all. However, if the ROBOR rate exceeds 2 per cent, then the tax rate amounts to 0.1 per cent of the value of assets of individual banks and grows by 0.1 percentage points with each increase of the rates on the interbank market by 0.5 percentage points.

For example, with a quarterly average ROBOR rate of 3.12 per cent in 2018 Q4, the bank tax rate in Q1’19 will amount to 0.3 per cent of the value of banks’ assets. If the ROBOR rate and the size of the banking sector’s assets remained at a similar level for the next three quarters, then the total burden on the banking sector in the whole 2019 would amount to 1.2 per cent of the value of the sector’s assets.

In its present form, the bank tax is charged on banks’ total assets, according to the value at the end of the previous quarter. This means that the government bonds held by banks are not excluded from the calculation of the tax base.

Why ROBOR?

The Romanian government declares that making the rates of the tax dependent on ROBOR rates is meant to encourage banks to lower the latter, and, as a consequence, to reduce the cost of loans for households and businesses. In Romania variable interest rates, dependent on ROBOR rates, are commonly used in loans. However, variable interest rates are applied to a much wider range of loans granted in the domestic currency, including not only housing loans and loans for enterprises, but also consumer loans.

The representatives of the Romanian government have expressed the view that ROBOR rates may have been inflated by the banks. Indeed, in the year preceding the introduction of the bank tax ROBOR rates increased sharply, and at the time of its announcement the spreads between the reference rate of the BNR (the repo rate) and the ROBOR 3M and 6M rates in 2018 were the highest among all the Central and Southeast European (CSE) countries. The interest rates paid on loans also increased following the increase in ROBOR rates.

However, the fluctuations in ROBOR rates are, to a large extent, a consequence of the liquidity situation in the Romanian banking sector and the liquidity management policy pursued by the BNR. As a matter of fact, liquidity was in the past a subject of technical assistance from the International Monetary Fund (IMF). When in the years 2015-2017 the Romanian banking sector experienced excess liquidity amid the increased inflow of EU funds, the BNR was carrying out liquidity absorbing operations with a yield equal to the deposit rate, and not to the reference rate (the repo rate). As a result, the interest rates on the interbank market, including ROBOR rates for all maturities, dropped to the lower regions of the BNR’s interest rate corridor. By the end of 2017, the situation reversed, which resulted in an increase of ROBOR rates above the repo rate. At the same time, the BNR raised the repo rate itself due to an increase in inflationary pressure amid high economic growth resulting, among other things, from the growing social spending of the Romanian government.

In late 2018 and early 2019, ROBOR rates fell once again, although they remained close to the repo rate. Some of the commentators found that this was a direct result of the introduction of the bank tax. However, another probable explanation is also a renewed increase in liquidity in the banking sector associated with an increase in the inflow of EU funds, as well as the possible conclusion of a series of repo rate increases by the BNR in light of the weakening of economic growth. In this period, the central bank mainly utilized liquidity-absorbing operations, but this time both with a yield equal to the deposit rate and to the repo rate.

Complications in the decision-making process

Linking bank tax rates with ROBOR rates would therefore introduce an indirect dependence between the banks’ fiscal burdens and the actions of the central bank. This has a number of consequences, which have repeatedly been pointed out by the BNR, including in the summary of the discussions at the January and February decision-making meetings, and during the hearing of the BNR’s Governor in the Romanian senate.

Firstly, the new tax complicates the central bank’s decision-making process, thereby making it less flexible. The BNR will have to take into account the greater sensitivity of the banking sector to interest rate changes in its decisions regarding the level of interest rates, as well as in its open market operations or deposit and loan operations. According to the BNR, this may have a negative effect on the central bank’s ability to keep inflation close to the target. This is all the more important if we consider, that — as has been pointed out by a representative of the central bank — in the past the BNR was forced to raise interest rates in order to limit the scale of currency depreciation, among other things in connection with an increase in the country’s risk. That was probably associated with the relatively large role of exchange rate stability in the monetary policy strategy pursued by the BNR, which is indicated by the low exchange rate volatility in relation to the euro, compared to other CSE countries.

Secondly, the new tax could reduce the effectiveness of the monetary policy transmission mechanism. This will be the case if in the process of determining ROBOR rates banks will be guided, even in part, by concerns about increasing their own fiscal burden. In such a case the changes in the BNR’s interest rates would have a smaller effect on the level of ROBOR rates and, consequently, on the cost of credit in the economy. Moreover, there are also other factors which could result in lower monetary policy effectiveness, including a possible decline in lending, a deterioration in banks’ liquidity position, a possible increase in the share of foreign currency loans, as well as an increase in margins and fees.

Thirdly, the BNR suggests that the Romanian government may be attempting to limit the independence of the central bank by attempting to influence market interest rates and by making public statements concerning their desired level. Certain statements of the representatives of authorities have already pointed out such intentions.

Lower profitability

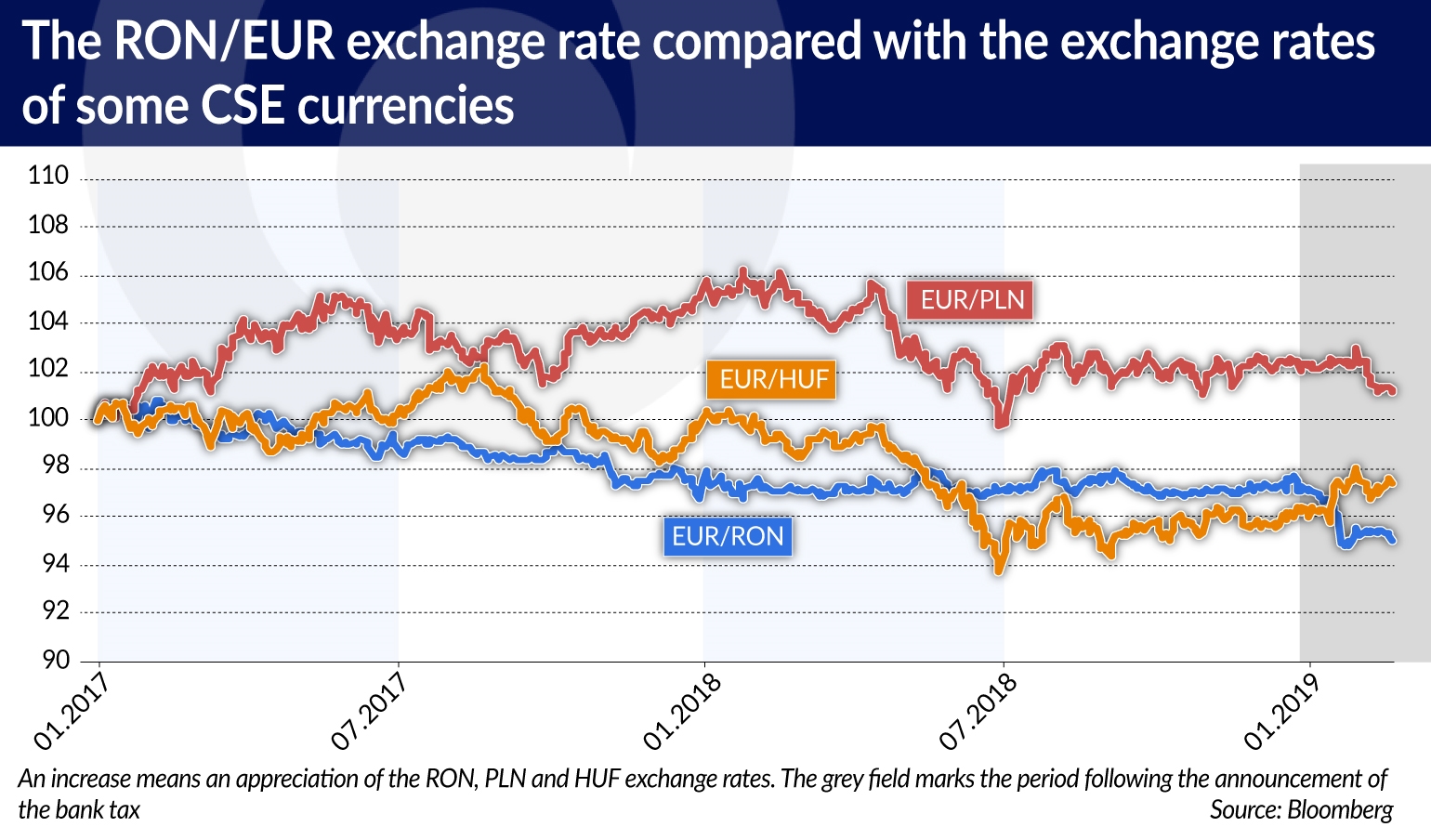

The Romanian financial markets have reacted quite strongly to the announcement of the principles of the newly introduced bank tax. The Bucharest Stock Exchange (BSE) index dropped by 18.5 per cent by the end of January 2019, and the stock prices of the largest publicly traded Romanian bank, Banca Transilvania, fell by as much as 33.2 per cent.

![]()

Also the exchange rate of the RON weakened by 2 per cent in relation to the EUR, as a result of which it fell to the lowest level in history. During that time, both the currencies and the stock indices of other countries of the region remained relatively stable.

The strong market reaction was associated with both the controversy regarding the possible weakening of monetary policy effectiveness as well as the concerns about a decline in the banking sector’s profitability following the introduction of the new tax. At the end of 2018, the value of the assets of the Romanian financial sector amounted to RON486.13bn. With a tax rate of 1.2 per cent, and under the assumption of an unchanged value of banks’ assets, this means that in 2019, Romanian banks would pay RON5.83bn in tax, which would be the equivalent of 83.3 per cent of the banking sector’s profits and 0.6 per cent of the Romanian GDP in 2018. Even with the somewhat more cautious estimates of the Romanian government (0.4-0.5 per cent of GDP and 54.1-67.7 per cent of the banking sector’s profits), this would still be the biggest bank tax burden among the CSE countries. In Poland, the budget revenues from the tax on certain financial institutions accounted for 28.6 per cent of the banking sector’s profits on average in the years 2016-2017, while in Hungary they accounted for less than 10 per cent of the sector’s profits.

As soon as the government in Bucharest announced its intention to introduce a bank tax, the Romanian central bank published a preliminary estimate of the consequences of the new tax burden. These calculations indicated that the majority of Romanian commercial banks may not even achieve a profit in 2019. In the final version of the bank tax legislation, the maximum tax rates tax are slightly lower and thus less painful for the banking sector. However, in the case of some banks, the size of the tax burden may still be several times higher than the amount of profits. The potential risks for the stability of the financial sector resulting from the new tax were indicated in the annual report prepared within the framework of the so-called European Semester by the European Commission, and also in the letters to the Romanian government prepared by the European Central Bank (ECB), as well as the International Finance Corporation and the European Bank for Reconstruction and Development (EBRD), which hold stakes in Romanian banks.

The bank tax is not the only solution that could affect the profitability of the Romanian banking sector in the near future. This is because the Romanian authorities have also announced their intention to introduce other, additional solutions burdening the banking sector, such as upper limits for interest rates on loans to households, for penalty interest, and for commercial banks’ claims arising from non-performing loans.

Other (un)intended consequences

The bank tax could also trigger unintended consequences in the form of an increase in the share of foreign currency loans in banks’ portfolios — for example, due to the depreciation of the RON. Foreign currency loans now account for 31.2 per cent of the banks’ credit portfolio and are still offered by banks. However, the degree of euroization of the Romanian economy is quite significant (37.2 per cent of deposits are denominated in the EUR), which means that even a stronger depreciation of the RON should not be a problem on the scale of the entire banking sector. Still, it could turn out to be painful for the borrowers with lower income buffers and those deprived of deposits denominated in the EUR.

There are also other potential challenges. Since the tax is charged on the total assets, banks may seek to reduce their tax liabilities by selling off some of the government bonds in their portfolios (according to data from the Romanian Ministry of Finance, banks hold 48.4 per cent of the bonds in circulation). Additionally, the Romanian authorities have simultaneously carried out a reform of the pension system, which will result in a significant reduction of inflows of funds to the capital pillar of the pension system, which holds approximately 16.5 per cent of the government bonds.

The representatives of the Romanian government initially claimed that one of the goals of the introduction of the bank tax is to reduce banks’ exposures to government bonds, which has been excessively high, according to the IMF. However, at the end of February 2019, the Romanian authorities began to consider the possibility of excluding certain assets, such as government bonds, from the tax base.

Banks should prosper anyway

However, all these objections should be viewed through the prism of the good condition of the Romanian banking sector, which was reflected in subsequent analyses carried out by the IMF. It cannot be ruled out that the profitability of the Romanian banking sector will return to the levels recorded prior to the introduction of the tax, following a decline in the adjustment period. However, banks may seek to compensate for the increase in their tax burdens by raising their fees and margins. The high probability of such a scenario has been indicated by the representatives of the BNR. The first signs of an increase in loan margins are already there — since the beginning of the year eight Romanian banks have increased them by 0.25 to 2 percentage points.

The representatives of the BNR also emphasize that the adoption of the value of banks’ assets for the calculation of the tax base may discourage commercial banks from expanding their lending. The experiences of other countries that have introduced similar taxes suggest that such effects do not have to necessarily occur if the economy is in good condition. Moreover, the available information indicates a low sensitivity of lending in Romania to changes in borrowing costs. In 2018, lending growth accelerated despite the higher cost of loans and the beginning of an economic slowdown. Meanwhile, the surveys carried out by the BNR and the European Investment Bank, as well as the analyses of the IMF, indicate that less than half of the companies in Romania use credit at all.

However, the controversy over the banking tax in Romania is considerable — it concerns both the adverse effects of the new tax on the conduct of the BNR’s monetary policy, and on the stability of the local financial system. It may also turn out that the revenues from the bank tax will be lower than initially estimated, as a result of a decrease in ROBOR rates.

The views expressed in this article are the private views of the author and are not an expression of the official position of the NBP.