European politicians debated the idea of a common currency as early as in the 1970s. The fluctuations in the exchange rates of the individual national currencies were an obstacle to trade in what was then known as the European Economic Community (EEC). On March 13th, 1979 the EEC member states introduced the Exchange Rate Mechanism (ERM).

EEC members agreed to keep the exchange rates of their currencies within a narrow band, which was referred to as the “currency snake”. The national currencies were allowed to fluctuate within the range of plus or minus 2.25 per cent from the established parity rate in relation to the accounting unit ECU (European Currency Unit). The name of the ECU was a reference to a medieval French gold coin, but it was only a unit of account.

The objective of the ERM was to limit the volatility of the exchange rates. But the participation in the mechanism was voluntary, and departure did not cause serious consequences for the EEC economy. The United Kingdom withdrew from participation in the ERM in September 1992, unable to resist the speculative attack on the British pound carried out by the hedge funds of George Soros. Meanwhile, Italy suspended its participation in the same year. In turn, the currencies of Spain and Portugal were devalued in 1993.

A leap into the unknown

The ERM stabilized the exchange rates, but the member states had sovereign central banks thus a sovereign monetary policy. Investors had to take into consideration the risk of individual countries leaving the ERM. Because of that, significant differences persisted between the countries belonging to the ERM in terms of the government bonds’ yields, the general level of interest rates, and also the level of inflation. For example, in the years 1990-1995, the yield of Italian government bonds was 3 to 6 percentage points higher than that of German bonds. The ERM provided an answer to the problem of exchange rate volatility, but it seemed to be too weak a response.

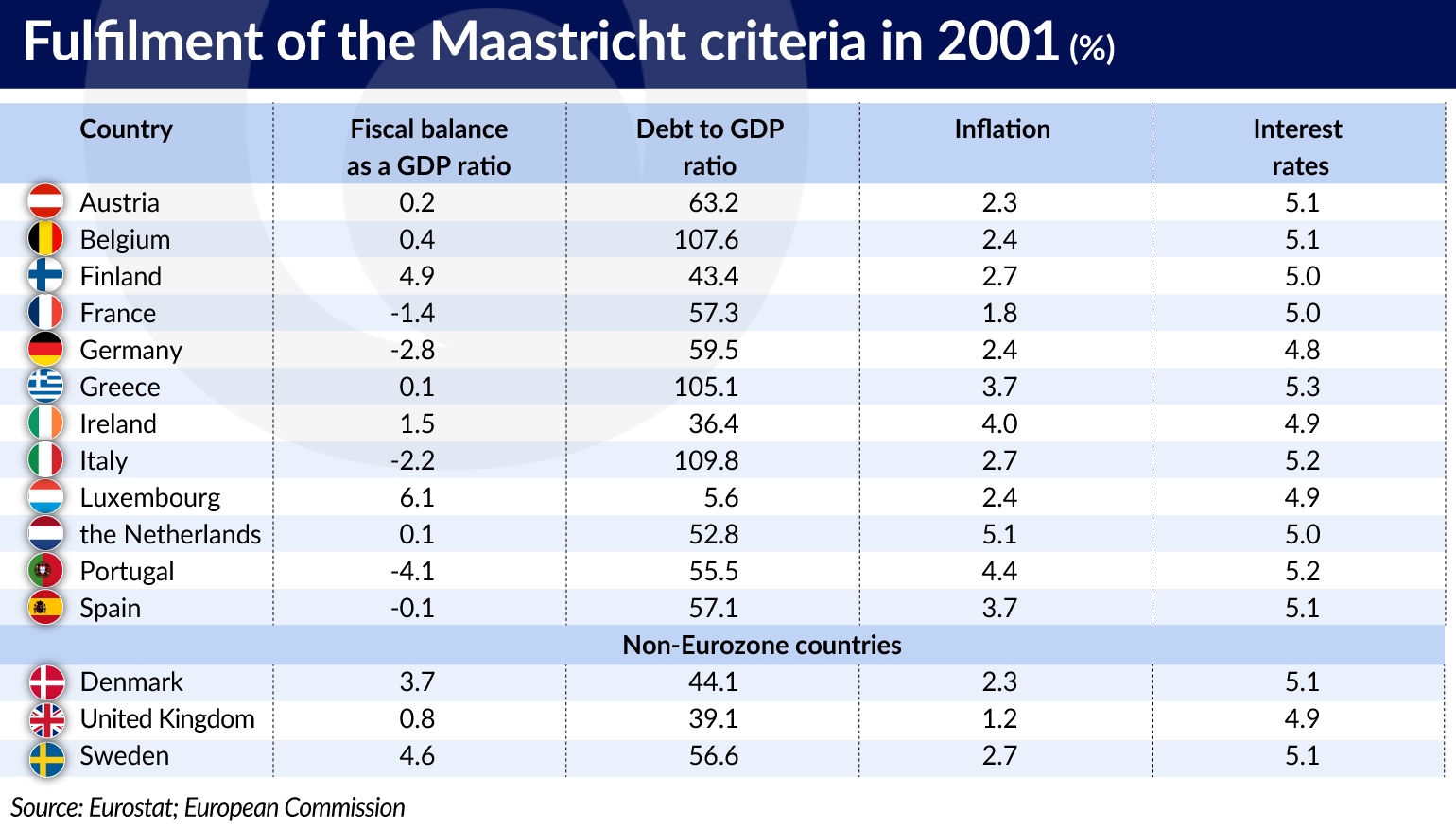

The establishment of a single currency for the European Union was decided in the Maastricht Treaty of 1992. In order to participate in this currency, the individual member states were supposed to meet the relevant criteria. Their budget deficit should be lower than 3 per cent of GDP and their public debt should be lower than 60 per cent of GDP. Meanwhile, their inflation should be no higher than 1.5 percentage points above the average inflation rate of the three EU member states with the lowest inflation, while the long-term interest rates should be no higher than 2 percentage points above the average rates in the three countries with the lowest rates.

In the Maastricht Treaty, the United Kingdom and Denmark were allowed to remain outside the single currency area. Other countries, including those that joined the EU after 1992, are required to adopt the EUR, although it is not determined when that will happen.

The name “euro” was officially adopted in Madrid on December 16th, 1995, thereby replacing the ECU. After that, all the EU countries, with the exception of the United Kingdom and Denmark, decided to jump into the pool without checking if there is any water in it. Sweden joined the European Union on January 1st, 1995 and found itself among the countries that have not adopted the EUR.

The Maastricht criteria were determined arbitrarily. They were not derived from any specific laws of economics, but from common sense. Countries that want to sell their bonds denominated in the single currency cannot have excessive debt or inflation that is too high. The problem is that some of the countries that were invited to the euro zone did not fulfil the Maastricht criteria. In 2001, Austria, Belgium, Greece and Italy all had a public debt exceeding 60 per cent of GDP. Portugal had a deficit greater than 3 per cent of GDP, while in Greece, Ireland, the Netherlands, Portugal and Spain inflation was too high.

It was generally assumed that the savings made on debt servicing costs as a result of the equalization of interest rates would be used to reduce the public debt. Because of that, countries that had clearly failed to meet the Maastricht criteria were allowed to participate in the euro zone. This was the case with Greece, which entered the euro zone with a delay, on January 1st, 2001.

The common currency was introduced on January 1st, 1999 in a non-physical form (traveler’s checks, electronic transfers, banking, etc.). The banknotes and coins of the national currencies were used as legal tender until the introduction of the new EUR banknotes and coins on January 1st, 2002. However, the conversion rates between the national currencies and the euro were already fixed and did not even have a narrow fluctuation margin.

The expected benefits

It was expected that the introduction of the single currency would accelerate the rate of growth of the European Union economy, which was supposed to happen through three channels. The first of these channels was supposed to be trade within the Eurozone (and generally within the European Union), which was expected to grow rapidly thanks to the elimination of the exchange rate risk. This also applied to trade in services, including tourism.

The common currency was supposed to encourage travel. Before the introduction of the EUR, the national currencies were already fully convertible and it was possible to determine the exchange rate of one against the other. However, only the determination of prices in a single currency in different countries allowed a proper comparison of what is cheaper and what is more expensive. Trade exchange was supposed to contribute and probably did contribute to price convergence.

The second channel was supposed to be the expansion of the market and the resulting increase in competition.

Finally, the third channel was supposed to be the reduction in interest rates, especially in countries that had a long tradition of high inflation and high public debt (such as Italy), and therefore also had high interest rates. The common currency area facilitated capital flows, which was beneficial for the less affluent countries including Spain, Greece and Portugal.

The calculations carried out before the introduction of the single currency clearly specified the increase in GDP growth that would take place through each of these channels. These expectations have not been fulfilled, however.

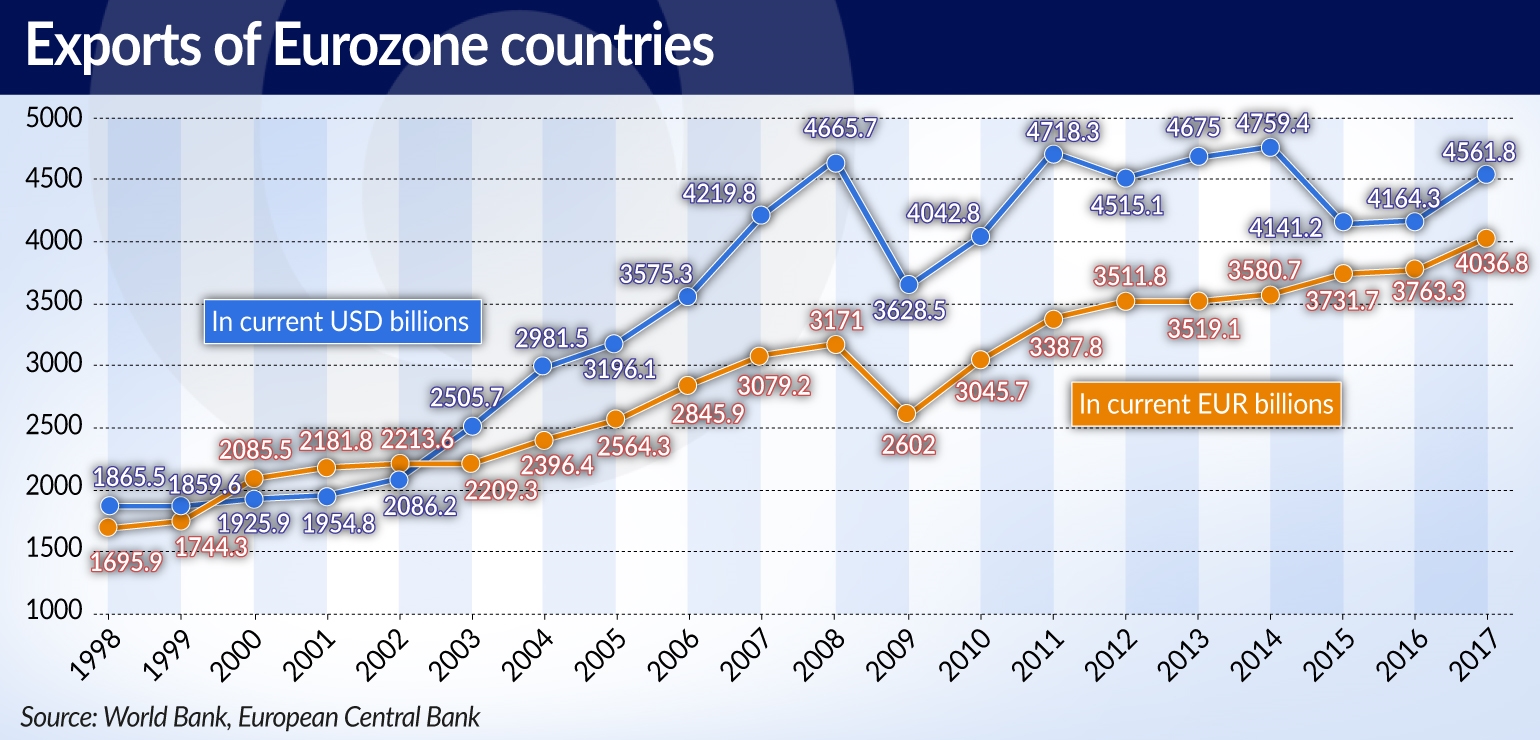

In the years 1999-2008, the average nominal growth rate of exports, expressed in current EUR, amounted to 6.5 per cent (own calculations), which was not a particularly impressive result in light of the fact that during this time the average inflation (measured by the GDP deflator) reached 2.9 per cent.

Moreover, contrary to previous expectations, trade within the Eurozone grew at a slower pace than trade between the Eurozone and the non-Eurozone countries. While in 1999 about 53 per cent of imports of Eurozone countries came from other member states of the Eurozone, and 50 per cent of their exports were directed to Eurozone countries, in the subsequent years these shares were decreasing. By 2014, trade within the Eurozone accounted for approximately 45 per cent of the total trade exchange of Eurozone member states.

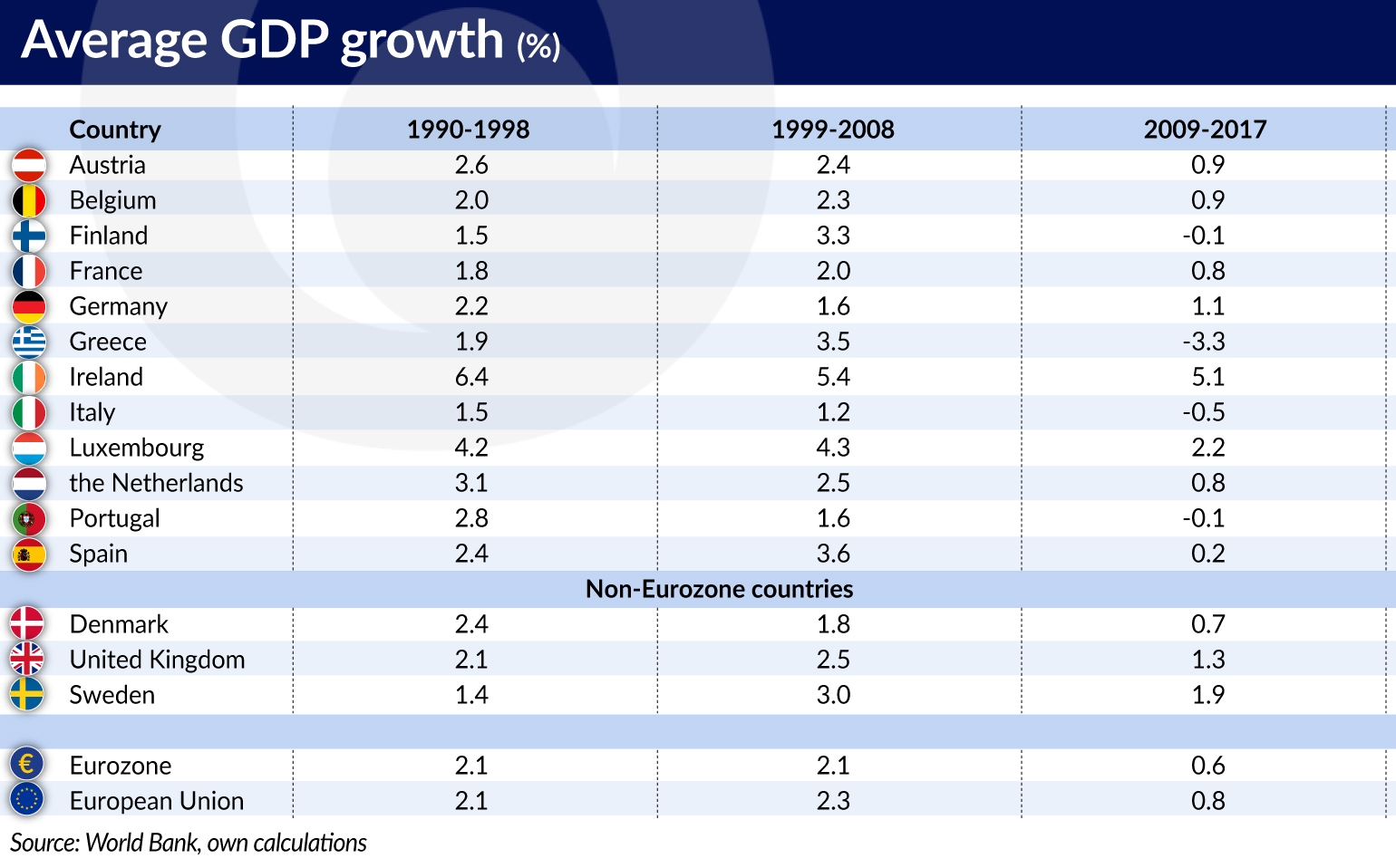

The expected increase in the rate of GDP growth also did not materialize. The average rate of GDP growth in the countries forming the Eurozone since 1999 amounted to 2.1 per cent in the years 1990-1998, and also 2.1 per cent in the years 1999-2008. The distribution of growth varied between the individual countries. A significant acceleration of growth occurred in Finland, Greece and Spain. Faster growth was also recorded in Sweden, which remained outside the Eurozone, and which went through a deep financial crisis in the 1990s.

Ireland, which had been expanding at an average rate of over 6 per cent in the 1990s, saw a slight softening of its growth rate, but it would be hard to associate that with the country’s entry into the single currency area. Simply put, the rate of growth of a country that is catching up typically decreases as it closes the distance to the wealthiest countries.

The creation of the Eurozone did not result in a significant increase or decrease in the rate of growth of the largest economies. Meanwhile, the economy of Germany slowed down. At the beginning of the century Germany was going through a serious crisis, which it was only able to overcome following the reforms carried out by chancellor Gerhard Schroeder. Growth in France accelerated slightly, while Italy’s economy grew as slowly as before that country’s entry into the Eurozone.

Among the countries that joined the Eurozone at a later point, the best results were achieved by Malta — in the years 2009-2017 its GDP grew at an average rate of 4.5 per cent. Meanwhile, the worst growth was recorded in Cyprus (+0.03 per cent) and Slovenia (+0.3 per cent). Slovakia, which adopted the EUR on January 1st, 2009, recorded an average rate of GDP growth of 2.1 per cent in the years 2009-2017. Meanwhile, the Czech Republic, which retained its national currency, achieved average growth of 1.4 per cent, and Hungary grew by 1.1 per cent on average. Croatia, which remained outside the Eurozone, recorded negative GDP growth during this time.

The above statistics indicate that it is difficult to conclusively determine whether the EUR has accelerated or slowed down GDP growth. Efforts to maintain the competitiveness of the economy through a more flexible labor market, better institutions and better conditions for entrepreneurship have proven to be much more important in this respect.

Imbalance

The country that suffered the most during the financial crisis was Greece, even though it had been among the most dynamically developing member states of the European Union prior to the crisis. Before entering the Eurozone, Greece had an average current account deficit of approximately 3 per cent of GDP. In 1999, this deficit increased to 3.6 per cent, and in the following year it reached almost 6 per cent.

The rapid economic expansion of Greece in the years 2000-2008 was driven by the inflow of foreign capital and high internal consumption. Both of these factors were related to the country’s entry into the euro zone. Investors saw Greece as a safe country, despite its high level of public debt, low exports and the fastest rate of increase in unit labor costs (the rate of growth in labor costs in relation to the rate of productivity growth) among the countries of the European Union. The Greek government did not take advantage of the lower debt servicing costs resulting from the decreased interest rates, in order to reduce the country’s debt. In 1999 it amounted to 98.9 per cent of GDP, while in 2000 it already reached 104.9 per cent. The increase in debt took place despite the fast rate of GDP growth. In 2007, on the eve of the global crisis, the debt of the general government sector in Greece amounted to 103.1 per cent of the GDP.

A similar situation occurred in Spain. Joining the Eurozone resulted in a decline in interest rates and an acceleration of the rate of GDP growth in that country. This means that the developments expected by the creators of the common European currency materialized. At the same time, however, imbalances were growing — in the case of Spain, a speculative bubble developed on the real estate market.

It probably would have been possible to reduce the risk of crisis in the Eurozone if the previously introduced regulations had been effective. However, the European Commission did not react when Germany and France maintained a fiscal deficit exceeding 3 per cent of GDP for a number of years. It also didn’t push Greece and Italy to reduce their public debt. The regulatory weakness and the inability to enforce the obligations arising from the Maastricht criteria became the main cause of the crisis.

An optimum currency area

In the 1961 book entitled “A Theory of Optimum Currency Areas”, Robert Mundell wondered about the conditions of functioning of a currency zone composed of many countries. There is a problem concerning the reaction to asymmetric shocks. In a common currency area, individual countries cannot conduct a sovereign monetary policy and cannot devalue or reevaluate their currency in response to an external shock. Mundell noted that the free movement of capital and people could provide an effective response to such a shock.

If one member country suffers as a result of a negative demand shock (e.g. Spain) and another faces a positive demand shock (e.g. Germany), then profits and wages will decrease in Spain and increase in Germany. These imbalances can be eliminated if both the employees and the capital move from Spain to Germany. This would ultimately lead to an increase in profits and wages in Spain and a decrease in Germany. The freedom of movement of capital and employees is guaranteed in the European Union, but while there are no problems with capital flows, the mobility of people is much lower, if only because of the language and cultural differences.

In his 1963 book entitled “Optimum Currency Areas”, Ronald McKinnon presented the thesis that the mobility of labor and capital in a common currency area is less important than the trade ties between the countries.

The theory concerning currency areas comes from Peter Kenen. In his opinion, asymmetrical shocks are not dangerous if production and exports are diversified. This means that an asymmetric shock only affects a part of the economy and, as a result, the shocks are dispersed. The countries of the Eurozone generally have diversified production, but not to the same extent. This certainly is not true in the case of the less affluent countries of southern Europe. Thus, the Eurozone does not meet the criteria of an optimum currency area.

The experience of the past 20 years shows that the single currency did not lead to a sustained acceleration of growth, although it did not hurt growth in countries with a sufficiently flexible economy and low level of debt. The actions undertaken by the European Commission and the European Central Bank made it possible to overcome the crisis, while the European Stabilization Mechanism, created on this occasion, became an institution conducive to the further integration of the Eurozone. Enforcement mechanisms were also introduced to ensure that countries maintain stable public finances. The reasons for the creation of the euro zone were mainly political and not economical, but today it is a permanent fixture, setting the tone for the entire European Union.