“Bitcoin is the ambassador of blockchain, but bitcoin cannot exist without blockchain, while blockchain can do without bitcoin,” says Piotr Barański of Deloitte Poland. According to Gartner analysts, in 2018 blockchain will be one of the six most intensively developed technologies in the world.

Blockchain – how does it work

Blockchain is a decentralized database based on open software developed by a community of programmers, in which there are no central computers and no centralized data storage location. It is used for the posting of individual transactions or, for example, accounting entries. The entries are encrypted using cryptography. On the one hand, blockchain provides the confidentiality of entries, and on the other, their openness.

Transactions are processed by computers connected in a network (known as nodes) and after validation, they are added to a replicated and time-stamped transaction log, known as the block chain. Each data block contains a specific number of entries with transactions.

In its present form blockchain is highly energy-consuming – it is estimated that one BTC transaction consumes as much energy as the average household in Poland in one month – and also relatively slow – it is estimated that the authorization of one transaction takes as long as the authorization of 8,000 credit card transactions settled through the Visa IT systems. In addition, adding each transaction to a block increases its size. This in turn means that storage of blocks requires more and more space on computer disks.

The improvement of all these parameters is one of the directions of development of this technology. Others include practical applications that go beyond trade in cryptocurrencies. And here the room for growth seems to be limited only by human imagination.

“This is not a technology which will provide a panacea for all the problems of our civilization,” says Ernest Frankowski, a partner at Deloitte Poland. He adds that we are still at the stage of finding new possibilities for its practical utilization.

The obvious applications include stock exchange transactions without the participation of intermediaries and institutions, trade in currencies and transfer of currencies, land and mortgage registers without their present form and without notaries, accounting books and share ledgers, all commercial transactions on the Internet, records concerning documents, including those we use on an everyday basis, e.g. medical records.

Blockchain in Poland

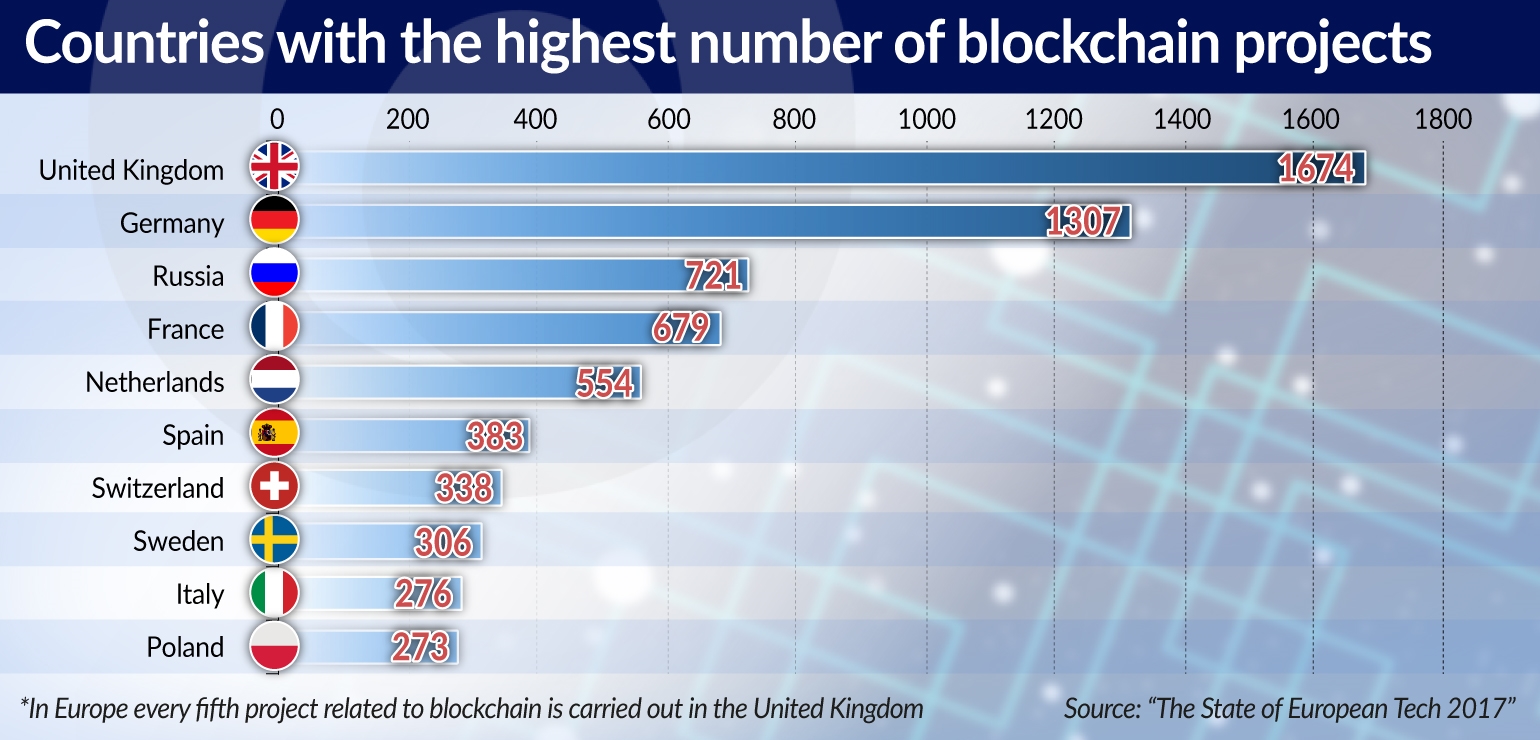

According to this year’s edition of the “State of European Tech” report prepared by the investment company Atomico, approximately 8,300 blockchain related projects are implemented in Europe, including nearly 300 in Poland. These projects are conducted both by financial institutions and enterprises, as well as companies for which the internet is the natural environment. Some projects are also implemented by the public administration, which is examining the possibility of practical application of the technology for the needs of the state.

Looking through the job offers from the last several months, we can discover that in Poland blockchain-developers, that is, programmers working with this technology, were being recruited by IT companies (including GTF Polska, a supplier of software for financial institutions; the Poznań-based company Espeo Software, whose offer includes software for conducting Initial Coin Offerings (ICO), i.e. issues of new cryptocurrencies; and the Kraków-based company Pragmatic Coders), as well as companies operating in other industries, such as Kinguin, the X-Trade Brokers brokerage firm, and BNP Paribas. There are also job offers, including remote jobs or jobs involving relocation, from foreign IT companies and providers of outsourcing services.

Among IT companies operating in Poland, various activities related to blockchain are also conducted by, among others, Coinfirm, which is expanding a platform supporting the adaptation to legal regulations and the combat against money laundering. The e-commerce startup Trivial, as well as GetLine, which offers a platform for social loans, use blockchain and virtual currencies in their business model.

“We are preparing two projects based on blockchain: a sales platform for games and accessories accompanying them, and the issue of our own cryptocurrency,” says Viktor Wanli, the CEO of the company Kinguin. “Blockchain technology allows us to track transaction history. This is very important in the sales of virtual products. Thanks to blockchain, we can easily check to whom the given product belonged before and after the transaction.” Kinguin decided to employ blockchain-developers in the company instead of relying on the servicers of an external company.

“Both variants have their advantages and disadvantages. An external company is a team of specialists, and therefore a customer can depend on the sum of their experience. In practice, however, outsourcing requires a lot of time for communication between the service provider and the customer. When the latter wants to change the scope of cooperation, time is required for negotiations, changes in the contracts, determination of new remuneration rates,” says Viktor Wanli, explaining the choice of the business model. He adds that blockchain is a long-term project.

“That’s why an employee on board will be a better choice. This will enable us to react on the spot. A developer will be a permanent part of the team, he will participate in decision-making processes and will simply be more effective than an external company,” says Wanli.

Financial sector as the main beneficiary

Today one of the largest stakeholders in the blockchain technology is the financial sector. This includes both banks and financial institutions, as well as companies classified as fintech, that is, young technology companies that want to use new technologies and business models to break the monopoly of competitors from the old world.

Big banks and companies providing financial services were the first corporate entities that decided to make direct investments in companies dealing with blockchain says CB Insight, a company involved, among others, in gathering data about the start-up market.

It is estimated that from June 2014 to October 2017, the 10 largest American banks invested at least USD270m in such companies. According to experts, financial institutions are using these investments to experiment with the practical application of this technology.

The consulting firm Accenture claims that thanks to blockchain, by 2025 the world’s largest investment banks will be able to reduce the infrastructure and back office costs by 30 percent, each of them saving USD8-12bn. Additional benefits include improved data quality and data transparency. Accenture emphasizes that the estimates do not take into account the implementation cost of blockchain technology.

The list of the five companies that most often invested in start-ups dealing with this technology in the years 2012-2017 (data until the beginning of October 2017) include Citigroup and Goldman Sachs. This shows how interested banks are in the blockchain. Apart from them, the list includes SBI Holding (which operates in the financial services, technology management and biotechnology sectors), Google and Overstock.com (which is involved in e-commerce). In Poland, PKO BP admitted to testing such technology.

What banks can gain from blockchain is well illustrated by the Utility Settlement Coin (USC) initiative, whose aim is to introduce a form of digital money that will allow for the settlement of financial transactions between their participants. The project was launched in 2015 by the UBS bank and the technological start-up Clearmatics Technology. It was later joined by subsequent banks, including Credit Suisse, Barclays, HSBC, Canadian Imperial Bank of Commerce, Banco Santander, BNY Mellon and Deutsche Bank. The project has entered the phase of conducting tests in the banking environment that will last approximately 12 months. The first transactions with the use of this technology are expected at the end of 2018.

Another company interested in blockchain is Mastercard, which offers a money transfer service using this technology. Here, however, the transfers are not based on a cryptocurrency, as is the case with the Utility Settlement Coin, but on traditional money. Mastercard justifies this with potential legal and regulatory problems.

SWIFT (Society for Worldwide Interbank Financial Telecommunication), the international association of financial institutions that maintains the telecommunications infrastructure used for exchanging information between banks, is also working on its own blockchain. The project initiated in early 2017 with the participation of 22 banks has the objective of checking whether this technology will be useful in international settlements in near-real time. This is a reaction of that organization to the activities of the banks which want to use blockchain to significantly reduce the duration of international transfers (in the current SWIFT infrastructure they take one or two days).

IBM also has an offer for banks. Together with the company Stellar it has announced the launch of a platform handling the international transfer of money between banks operating in the South Pacific region. The platform will use blockchain and a cryptocurrency called Lumens. There are 13 banks participating in the project. IBM expects that in the first quarter of 2018, 60 percent of foreign transfers between the participants of the project will be carried out through the platform.

ASX, the largest stock exchange in Australia, made an important decision at the beginning of December 2017. After two years of testing, it decided to replace its existing clearing and assets registration system with a blockchain-based solution. According to Dominic Stevens, the CEO of ASX, the change of technology will enable a reduction of the costs borne by exchange participants and the launch of new services. The new system, supplied by the American start-up Digital Asset, which has been operating since 2014 (over USD115m was invested in that company by ASX, Goldman Sachs, JPMorgan Chase, CME Group, Deutsche Boerse and Citigroup, among others), is expected to launch operations in March 2018.

Energy eyes blockchain

Another initiative involves a plan for the creation of a blockchain-based platform for settling trade in energy resources. The project brings together oil companies (BP, Shell and Statoil), companies involved in trade in commodities (Gunvor, Koch Supply & Trading, and Mercuria), as well as banks (ABN Amro, ING and Societe Generale). The platform, which is ultimately supposed to be open to producers of energy commodities, should be launched by the end of 2018. Its advantages are to include the minimization of operational risk and reduction of transaction costs.

Outside of the financial sector, blockchain-related projects are carried out by IBM and Toyota. IBM has offered the authorities of the Canadian province of British Columbia the use of solutions based on this technology for the control and supervision of the legal production and marketing of marijuana. Meanwhile, the German electricity transmission system operator TenneT is implementing a solution using the IBM blockchain platform, which will enable the remote decentralized management of charging and emptying of storage systems for energy produced by wind and solar power plants. In turn, Toyota is planning to use blockchain to track components used in car production in the supply chain.

The Korean government is financing trials of the utilization of blockchain for settlements between the private domestic producers of solar or wind power and their neighbours using the surplus production. In turn, the authorities of Seoul want to implement this technology by 2022 for the management of public transport and security in the city, as well as for the collection of all the legally required information about residents.

Other sectors can also use blockchain

Don Close, analyst at Rabobank, claims that this technology could find wide application in agriculture. He provides the examples of tracking cattle movement, trade in cattle and recording who was and is the owner. For the time being, it is used in the wool trade in Australia.

Deloitte is convinced that solutions using blockchain can also be used for the collection of payroll taxes and in VAT settlements. However, it is expected that the tax collection technology will be applied no earlier than in five years.