Tydzień w gospodarce

Category: RaportyPrzegląd wydarzeń gospodarczych ubiegłego tygodnia (16–20.05.2022) – źródło: dignitynews.eu

It has already seemed that the Capital Markets Union (CMU) project would fade away soon after June 23rd, when the British voted to leave the European Union. On top of that, Lord Jonathan Hill, who resigned soon after the UK referendum on EU membership, was in charge of the project. However, the European Commission considered those circumstances as only temporary organizational problems.

The long-lasting effects, attainable despite Brexit, or maybe even thanks to it, are more important. After the Commission Action Plan concerning the CMU project was established in September, the EC called on the Council, the European Parliament and Member States to accelerate efforts aimed at its implementation.

“This plan is more important than ever and the implementation of actions in the plan should be accelerated. It is crucial that all relevant actors work together to achieve this,” the EC wrote.

Jonathan Hill was involved in the CMU project for several reasons. First of all, the intention was, among others, to increase the integration of the City of London with continental Europe. Although the banking sector is also ‘overgrown’ there as in many other countries of the Continent, only in the UK is the model adopted for financing of the economy closer to the American one, where companies more often than borrowing funds from banks raise capital on the stock or debt market. And this is exactly the goal of the capital markets union – to enable and improve non-banking financial intermediation mechanisms in view of the weaknesses of the banking sector.

The banks’ weakness resulted in considerable shrinking of internal capital flows in the EU after the crisis. According to Filip Keereman of the EC Directorate General FISMA, in 2013-2014 they dropped by 25 per cent in relation to the period of 2005-2006.

“The project should eliminate barriers to growth in the cross-border flow of capital and investment,” said Filip Keereman at the Annual NBP Conference on the Future of the European Economy held in mid-October in Warsaw.

London could have been the greatest beneficiary of the CMU project for several other reasons. It is the place of operation of institutions (also from America and continental Europe) with great know-how in the scope of creating complex financing. Contracts for financing are usually concluded under British law. This is also where the third stock exchange market in the world in terms of capitalization operates. Trade in almost all securities denominated in EUR is currently cleared in London.

Moreover, the CMU was a kind of revenge for earlier regulations imposed on the banking sector which significantly affected the City of London. This effect was quite a subjective feeling, because if we compare prudential regulations, in particular those related to consumer protection applied on the Continent and on the British Isles, the latter are frequently much more stringent.

Citigroup has already moved some part of its operations to Dublin due to capital requirements introduced by the Bank of England. Thus, it’s not surprising that a question has emerged on how the CMU should be built without the City. Paradoxically, it turns out that a totally new opportunity appears after Brexit.

“Without the potential threat of the British aversion towards deep integration, the project may now be more ambitious. The EU may build a real Capital Markets Union without the United Kingdom more effectively,” said Sven Giegold, the German MEP quoted by the Financial Times, immediately after the UK referendum.

So in September the European Commission announced the “acceleration” of the project.

The Capital Markets Union is a slightly misleading name. The project is not about the creation of one or even several fundamental institutions (as in the case of the Banking Union and the Single Supervisory Mechanism) or about issuing a single incorporation act of law. The Union will be based on 33 measures, mainly on the review of several dozen regulatory acts and the removal of barriers for financial intermediation so that the costs of raising capital by companies can be reduced.

“The aim is to create a more integrated European model of getting access to sources of finance. It is necessary to switch slowly to financing originating from the capital market,” said Debora Revoltella, director of the Economics Department at the European Investment Bank during the NBP conference.

At the same time, the goal is to expand the offer of collecting savings outside the banking sector, that is, in investment funds, pension schemes, and to facilitate cross-border investment, not only intra-EU, but also to attract higher-value direct foreign investment to the European Union. And, last but not least – the aim is to create opportunities for obtaining financial resources for long-term investment for the needs of the whole Union, e.g. connecting the states’ infrastructure.

Following the resignation of Jonathan Hill, the project may lose its ‘deregulatory’ and ‘liberal’ edge; however, there have already been earlier symptoms indicating that discussions will take into account the context of financial system security to a much greater extent than envisaged by the former commissioner. Instead of the banking sector, new sources of economic financing can be found in the shadow banking sector, whose assets exceed 250 percent of the EU’s GDP anyway, encouraging it to increase its involvement in financial intermediation.

The European Systemic Risk Board (ESRB) has recently emphasized the fact that the risk accumulated by this sector and the directions of its transfer are still poorly recognized. Thus, the proposals of far-reaching deregulation of the non-banking financial system after years of tightening of regulations for banks can hardly discourage arbitration, which takes place across Europe anyway.

In August the European Commission launched consultations concerning the new tasks for macroprudential supervision, among others, in connection with the CMU project.

“Sometimes the control of capital flows by macroprudential supervision is the best response to crisis,” said Jonathan Ostry, deputy director of the Research Department at the International Monetary Fund during the NBP conference.

Thus, the capital markets union may move in the direction of risk dispersion, through the multinationalization of capital and diversification of investors’ origin, as well as through increasing the availability of numerous instruments of analogical and transparent construction in many different markets. This is not the case of risk accumulation and its non-transparent, or even disguised transfer into unknown and difficult to identify areas.

The strengthening of prudential rules does not mean that solutions, which have prepared for some time, and assume much greater transparency, as well as take into consideration the needs of investors and the economy to a greater extent than so far, may not be introduced. Such is the case of the proposal to create a new model of simple, transparent and standardized (STS) securitization, based on rules once developed by the European Central Bank and the Bank of England. Currently the European Parliament is working on the EC proposal.

The EC September’s communication shows that this proposal attaches much greater importance to two areas of the reform identified as the most difficult. The first is the harmonization of the bankruptcy law in the EU. Its current ineffectiveness and differences in bankruptcy regulations result in investors’ legal uncertainty, hamper debt recovery by creditors and inhibit effective restructuring of companies. Simultaneously, the principle of “a second chance” for entrepreneurs going bankrupt will apply in Europe.

The second of the biggest challenges is the harmonization of tax law. The EC will probably focus on two aspects – an attempt to abolish the withholding tax in the EU member states and a change of the preferential tax treatment of debt over equity. This is how the tax systems operate in many countries, including Poland, and in the Commission’s opinion, capital investment should strengthen companies which will also generate financial stability benefits.

However, the EC will not give up on broader reform and the introduction of a common consolidated corporate tax base (CCCTB). Details of the proposal will be known as early as this autumn.

Besides the project related to securitization, the amendment to the Prospectus Directive is currently the subject of works at the EP level. Recently the EC announced the proposal to liberalize the provisions concerning small European venture capital funds – EuVECA (able to collect up to EUR100,000 from an investor) and European social entrepreneurship funds – EuSEF. The proposed amendments to the Solvency II Directive will reduce the capital burden for insurance companies investing in long-term infrastructural projects.

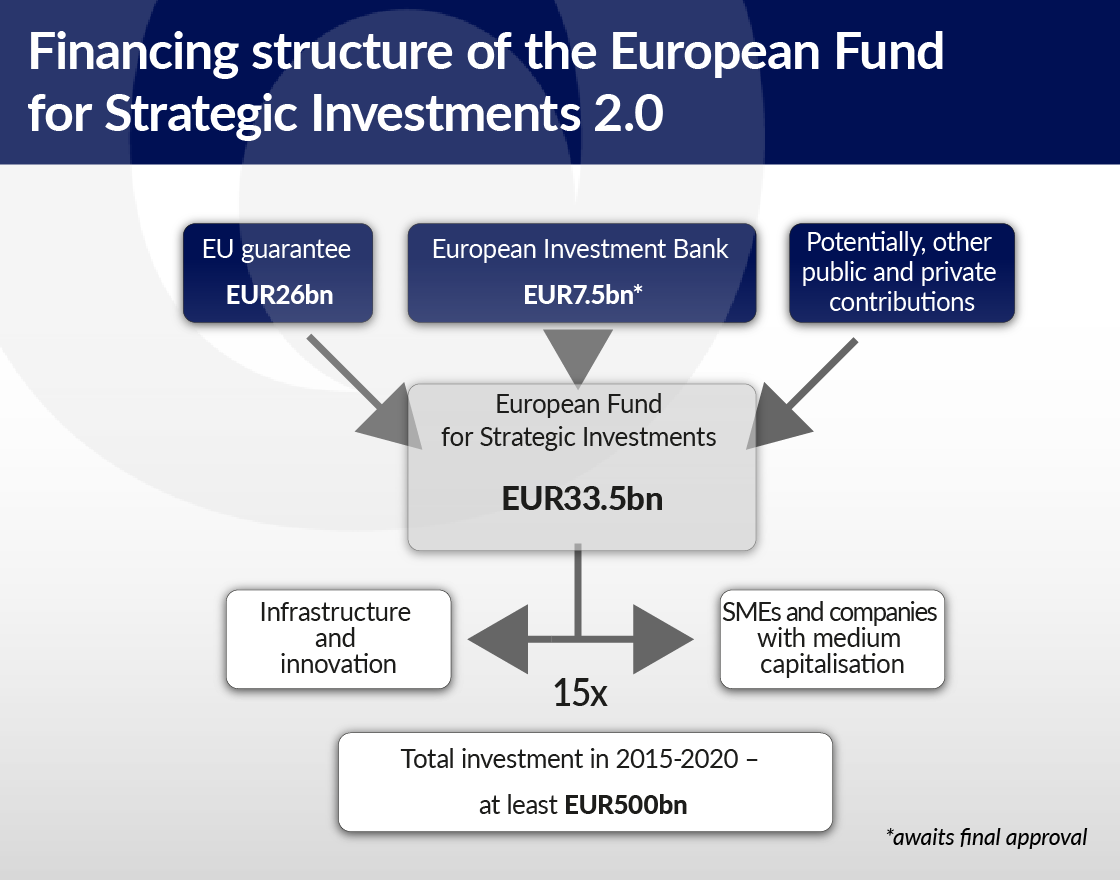

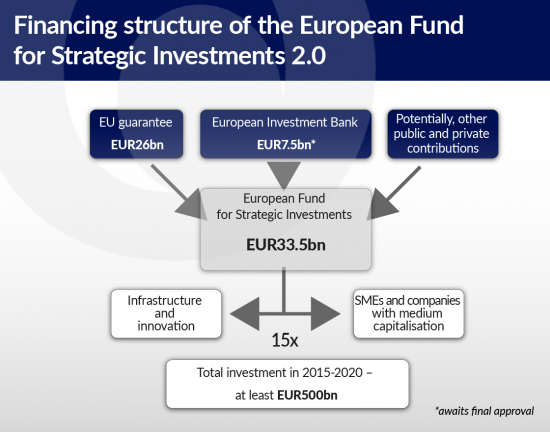

The most spectacular change showing the determination of the EC in introducing new mechanisms of economic growth stimulation is the announcement concerning the increase in investment capacity of the European Fund for Strategic Investments (EFSI) from EUR315bn to over EUR500bn and the announcement to extend its operations until 2020.

The EC informs that the current balance of demand for EFSI funds is its great success, since approx. 250 transactions in 26 EU member states have been approved, and the total investment should amount to EUR100bn, i.e. 32 per cent of the funds available to the fund. To date, nine projects with EFSI financing are to be implemented in Poland.

EFSI priorities include cross-border infrastructural investment, investment projects aimed at implementation of the climate agreement as well as financing of small and medium-sized enterprises. The EC has also established the European External Investment Plan (EEIP) with a value of EUR44bn, addressed to investment in Africa, in order to mitigate the reasons for economic migration.

The United Kingdom’s exit from the European Union will facilitate the discussion concerning an extremely significant issue, namely, the position of capital market supervision. It is obvious that the ESRB will play an important role; however, in accordance with the intention, the Securities and Markets Authority (ESMA) with its registered office in Paris will act as the microprudential supervisor. It would have probably been the subject of a dispute difficult to resolve, if not the results of Brexit referendum.

The fact that Vice-Chairman Vladis Dombrovskis, a Latvian and thus a representative of a small country from the “New Union”, became the “mentor” of the CMU project, should foster better representation of smaller economies’ interests, especially in view of the fact that Brexit will cancel the expected obligations of the CMU towards London. Anyway, it is likely that the financial centre will move from London to the Continent.

“We’ll work closely with co-legislators so we can progress quickly and make the CMU a reality,” said Valdis Dombrovskis, quoted in the EC communication in September.

The EC reiterates that the CMU is a project for all EU countries, although the capital markets in these countries are at various stages of development. It emphasizes that smaller companies need access to unobstructed local financing. Therefore, it proposed a program of technical support of reforms, to be used by all countries requiring knowledge on how their markets can be developed and improved.

As far as the position of Poland in relation to the CMU project is concerned, the interests of the Warsaw Stock Exchange would probably create the greatest problem. The reason is that considerable problems exist with its location on the map of Europe. Last year the number of companies leaving WSE was higher than the number of IPOs. Some of them, such as Work Service, transferred the trading of their shares to LSE.

The community around the WSE frequently expressed concerns that the European project would contribute to its marginalization, whereas the WSE aspires to become a regional centre and ‘drain’ the more attractive companies from other, smaller economies, which had been happening in the years of boom. A situation in which the Warsaw market has totally different interests from the ‘small’ players – such as the capital markets in Malta, Cyprus or even Slovenia – on the one hand, and the ‘great’ players – such as Euronext, Deutsche Boerse or Nasdaq OMX – on the other, can make it difficult for the WSE to fight for its interests on its own.