Tydzień w gospodarce

Category: RaportyPrzegląd wydarzeń gospodarczych ubiegłego tygodnia (16–20.05.2022) – źródło: dignitynews.eu

At the beginning of its economic transition, Poland, like several other Central and Southeast European (CSE), introduced a fixed exchange rate regime for the national currency. It was one of the anchors stabilizing the economy and curbing price growth. After several years, the shortcomings of the fixed exchange rate began to outweigh its advantages.

Even before the launch of market reforms, on March 1989, the last communist government legalized trade in foreign currencies. As a result, the market exchange rate of the USD — then the most important foreign currency in Poland — strayed considerably from the official rate as determined by NBP. Within few months, the Polish zloty was devalued several times. The market rate, which had fluctuated wildly in the autumn of 1989, began to stabilize. It was a good starting point for the unification of the exchange rate, which took place in January 1990.

An important decision, taken in cooperation with the International Monetary Fund (IMF), was the level of the exchange rate. The IMF called for the maintenance of a fixed rate for 12 months (and a minimum of three months), the Polish side proposed the adoption of a fixed rate for an unlimited period.

In January 1990, the m/m inflation was 79.6 per cent, and at the end of 1990 the 12-month inflation reached 249.3 per cent. Thus, prices increased nearly 3.5 times during a year, meaning that the pegging of the Polish zloty exchange rate resulted in a strong real appreciation of the Polish currency. Despite this, in 1990, Poland managed to achieve a positive trade balance and a surplus on the current account while the foreign exchange reserves of the central bank, NBP increased from USD2.5bn to USD4.7bn.

The stabilization of the exchange rate resulted in the initial undervaluation of the Polish zloty and the high interest rates on deposits and loans, which exceeded the inflation rate. The negative side of this was the inflow of short-term capital to Poland. Enormous profits could be made by exchanging the USD to the Polish currency and placing a deposit at a bank for a few months.

In 1991, the economy began to show the negative effects of the rapid appreciation of the Polish zloty — a devaluation was necessary. Although inflation had been falling, it still exceeded 50 per cent annually. With hindsight, it is clear that a reduction to single-digit levels would require much higher interest rates, which would have led to an even deeper recession.

In May 1991, the Polish zloty was devalued by 16.8 per cent, and in October 1991 the so-called crawling peg was introduced. The zloty was devalued every day against a basket of currencies in which the USD accounted for 45 percent, the German mark for 35 per cent, the GBP for 10 per cent, the French franc and the CHF for 5 per cent each. On a monthly basis, Polish zloty lost 1.8 per cent compared to the basket.

The advantage of the crawling peg was minimizing the exchange rate risk — entrepreneurs trading with foreign countries could anticipate the rate (in spite of a number of devaluations carried out besides the „crawling”) — and preventing its excessive real appreciation. The disadvantage was that the constant nominal depreciation of the zloty was itself one of the sources of inflation.

In subsequent years, the rate of „crawling” was reduced and the tolerance of the zloty against the basket was widened. From January 1999, the band was ±15 per cent, and the structure of the basket was changed – the EUR accounted for 55 per cent and the USD for 45 per cent.

Such a wide fluctuation band meant that zloty was nearly free floating. NBP strived to adjust its monetary policy to the shifts in the exchange rate policy. In 1996, NBP applied a version of monetary policy based on controlling interest rates. In 1997, it switched to controlling the size of the monetary base, and in 1998, the growth of the M2 monetary aggregate. However, these strategies did not succeed in reducing inflation to a sufficient level, required from the point of view of Poland’s accession to the European Union. In October 1998, twelve-month CPI inflation, for the first time since the beginning of the transition, fell to a single digit level of 9.9 per cent. In February 1999, it had dropped to as little as 5.6 per cent, which was partly due to smaller food exports to the Eastern markets. However, a new increase in fuel and food prices drove inflation back up to 11.6 per cent in July 2000. In this situation, an adjustment of the exchange rate policy and monetary policy was necessary.

The Monetary Policy Council (MPC), established in 1998, published a document titled „Medium-term monetary policy strategy for the years 1999-2003”. It read: „The central bank’s objective is to maintain a stable price level. This can be achieved using the strategy of direct or indirect inflation targeting.” And further: „The strategy of a direct achievement of the set inflation target will be implemented in the conditions of an increasingly floating exchange rate”.

One of the goals of floating the exchange rate and the introduction of direct inflation targeting was to prepare the PLN for the participation in the ERM2 exchange rate system, and subsequently for the adoption of the EUR by Poland.

After the PLN was floated, the exchange rate ceased to be a monetary policy instrument. In this situation, direct inflation targeting (DTI) became an obvious choice for NBP and the MPC. An alternative could be to permanently peg the PLN to one of the strong convertible foreign currencies, as it was done in the Baltic states and in Bulgaria. This would mean a waiver of sovereign monetary policy and hinging the struggle against inflation on an external anchor.

The DIT strategy assumes no intermediate targets. The central bank does not target a single indicator but instead takes into account all available information about any threats to the achievement of the inflation target adopted for the year. In implementing this goal, the NBP uses all available instruments of monetary policy. It is a transparent strategy. The MPC determines what level of inflation it seeks to achieve and maintain, and communicates it to the financial markets and the public.

In 1999, the inflation target was set at 8-8.5 per cent, and was later adjusted to 6.6-7.8 per cent. Annual inflation was 7.5 per cent, but in December 1999, 12-month inflation was at 9.8 per cent. In 2000, the inflation target was 5.4-6.8 per cent, and the annual inflation rate was 10.1 per cent. The failure of the efforts to combat inflation prompted the MPC to launch a more restrictive monetary policy. In August 2000, the refinancing rate was raised to 24 per cent and only in March 2001 a series of interest rate cuts began.

In 2001, for the first time the inflation declined and in the whole year it amounted to 5,5 per cent, to fall further to 1.9 per cent in 2002. Since 2004, the inflation target has been 1.5 to 3.5 per cent.

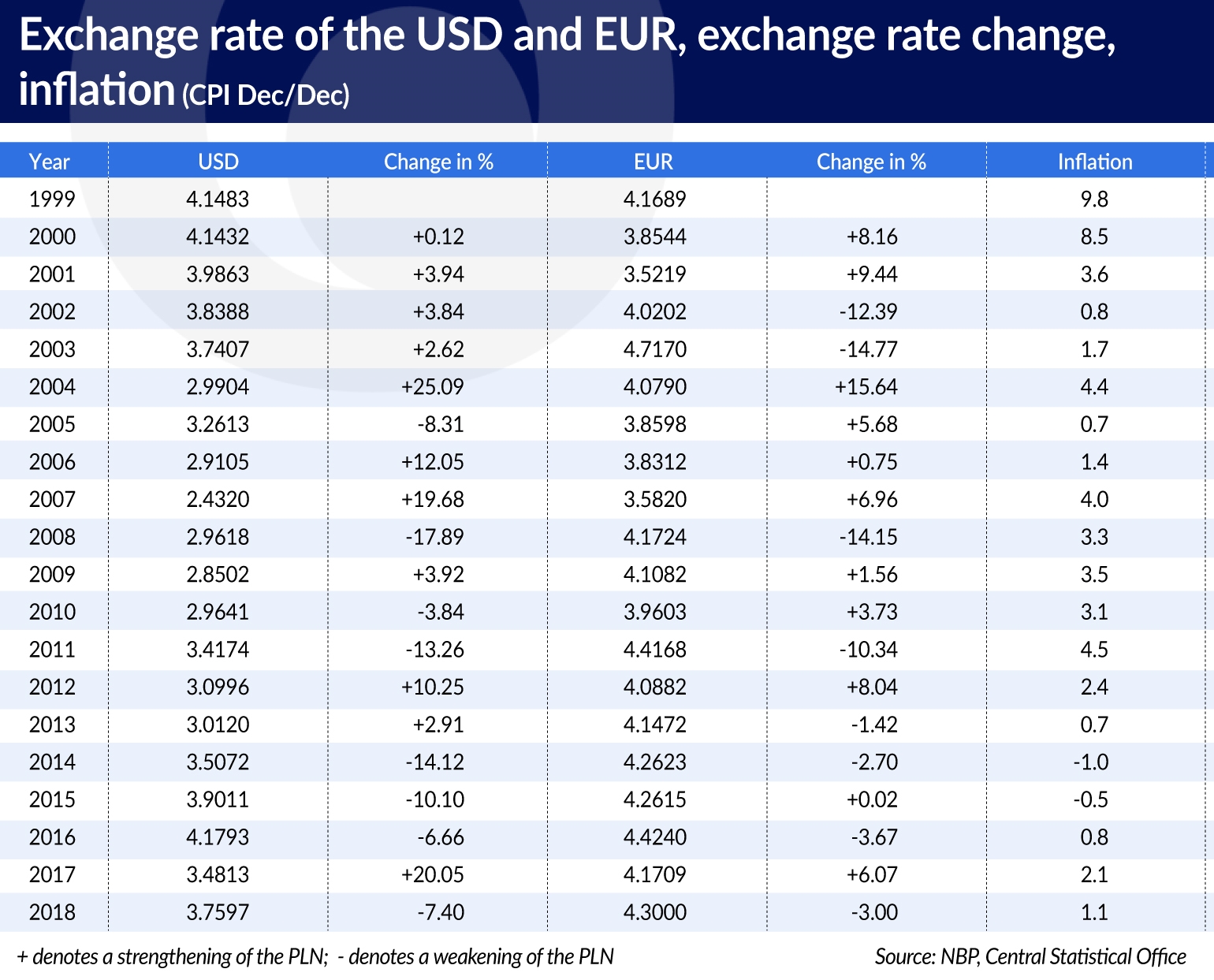

For four years — until the Polish accession to the European Union — the exchange rate fluctuated. The exchange rate of the European currency to the USD also changed. In 1999, the EUR was worth USD1.1, but the USD appreciated against the EUR. At the end of January 2000, for a short time, the USD had the same value as the EUR, after which the gap opened again.

These fluctuations had an impact on the PLN. The USD had been traditionally regarded as the main foreign currency in Poland, but its major trading partners were the European Union countries and the Eurozone.

The USD was at its most expensive against the zloty on 21 October 2000. Its NBP exchange rate amounted to PLN4.71. The EUR reached an all-time high in February 2004 — of PLN4.91.

The turn of 2003 was not too good for the Polish currency. The restrictive monetary policy of 2001 led to a slowdown in GDP growth, which in turn caused an increase in the budget deficit. The government implemented a program of consolidating public finance, the so-called Hausner plan, but it was only partly successful due to lack of a stable majority in the parliament. From the beginning of September 2003 till the end of February 2004, the PLN lost 11.5 per cent against the EUR. It lost only slightly against the USD, as at the same time the value of the US currency saw a sharp decline. Many players in the currency market were convinced that the ceiling of PLN5 per the EUR1 would be broken.

This sharp depreciation of the zloty at this time is difficult to explain. The theory of rational expectations states that economic entities make their decisions based on all available information about current economic conditions and the potential impact of these decisions. In June 2003, a referendum on a membership in the European Union took place in Poland — the date of official accession to the EU was already known. Investors must have known that after the abolition of restrictions on the movement of capital between Poland and West European countries, the Polish currency would strengthen. And yet, for a few months they played for its weakening.

After the official accession to the EU, the PLN, as predicted, embarked on a steep appreciation path. The appreciation continued (with some breaks) until the end of July 2008. In April 2004, just before the official accession, the exchange rate of the EUR at NBP was PLN4.7981. By the end of 2004, the PLN had gained 17.6 per cent, rising further by 5.7 per cent in 2005, 0.7 per cent in 2006 and 7 per cent in 2007. In July 2008, the EUR exchange rate was PLN 3.2026, which was a historical record. Within four years and three months, the PLN had strengthened against the EUR by almost 50 per cent.

Such a significant appreciation did not harm the Polish economy and exports, which, in terms of the current PLN increased by 49 per cent in the years 2004-2008, and by 95 per cent expressed in the EUR. Imports increased by 52.7 per cent and 99.6 per cent, respectively. The negative balance in trade in goods increased in that period from EUR11.7bn to EUR26.2bn, but rapid economic growth was maintained, and inflation remained within the target band.

The PLN was not the only currency in CSe to appreciate in the first years of the EU membership. The strengthening of local currencies was motivated by the so-called Balassa-Samuelson effect, which was described simultaneously in 1964 by two economists — Bela Balassa and Paul Samuelson.

According to their theory, emerging market countries pursue an accelerated growth strategy based on export expansion. The export-oriented sector is growing faster, which means that its labor productivity is growing faster than in sectors that do not participate in international trade. Productivity growth leads to wage growth, which occurs not only in the export sector but also in the rest of the economy. In the latter case, wage growth exceeds productivity growth, resulting in price increases that do not entail a corresponding depreciation of the domestic currency. Its exchange rate results from productivity in the export sector. Thus, the final effect is a real appreciation of the national currency.

In fact, Poland saw not only a real, but also a nominal appreciation. The Balassa-Samuelson effect triggered the inflow of FDI, as well as portfolio investments. Foreign funds, anticipating the strengthening of the CSE’s currencies, especially the PLN, invested in these countries, particularly as interest rates remained at a much higher level than in the USA or Western Europe. The benefits of investment were therefore double. The excessive inflow of short-term capital boosted the risk of a financial crisis. When the global crisis broke out, the countries with hard currencies were hit hardest. Yet the floating exchange rate of the PLN mitigated the external shock and was one of the reasons why economic growth in 2009 continued, while the rest of Europe was in recession.

From the beginning of August 2008 to March 2009, the PLN lost nearly 30 per cent of its value against the EUR and over 40 per cent against the USD. Of all the currencies of the European Union countries, the PLN lost the most to the EUR at that time. This was due to two reasons:

It is also worth noting that NBP, unlike other central banks in CSE region, very rarely used currency interventions.

The depreciation of the zloty resulted in an increase in the cost of debt servicing for the corporate and household sector (housing loans denominated in foreign currencies), an increase in the debt of the State Treasury, but at the same time an improvement in the trade balance. In 2009, exports of goods calculated in the current EUR decreased by more than 20 per cent, imports by 25 per cent, but exports calculated in the PLN increased by 4 per cent, and imports decreased by 7 per cent. The foreign trade deficit in goods decreased from PLN91.6bn to PLN40.1bn, which accounted for 3.8 per cent of GDP.

This, together with a significant fiscal stimulus, was the reason why Poland maintained its economic growth. Although foreign capital withdrew from Poland, it was not as massive as in countries with a fixed exchange rate. The increase in debt repayment costs was severe for households and enterprises, yet there was no wave of bankruptcies. The current account deficit fell to EUR12.6bn in 2009. In 2008, it amounted to EUR24.4bn.

After a significant weakening, the PLN rebounded in 2009, but the steady trend of appreciation did not return. In that period, the Polish currency was quite stable, especially in relation to the EUR.

The floating PLN had an increasingly strong backing in foreign reserves of NBP, which (expressed in the current USD) increased 27 times in 25 years.