We are seeing a return to the tendency to reduce tax burdens. In order to plug budget gaps, governments are hoping, among others, to improve the collection of VAT revenues. In this regard Poland is becoming an example for others to follow. Since the outbreak of the financial crisis in 2008 governments have had significantly less room for maneuver in reducing the tax burden for individuals and businesses. Enormous funds have been used to rescue banks and firms threatened with collapse and to finance the rise of social spending in connection with the increased number of the unemployed. The higher spending has led to increases in the ratio of public debt to GDP, which does not leave much room for tax reductions. Priority was given to consolidation and balancing of the financial systems.

The global economy’s return to growth (however weak it may still be) is once again changing the perspective on economic policy. In recent years the consolidation and balancing of public finances has led to an increase in the average tax burden. Within the OECD this is measured by the size so the so-called tax burden, i.e. the total amount of the taxes and other charges (such as social insurance contributions) in relation to GDP.

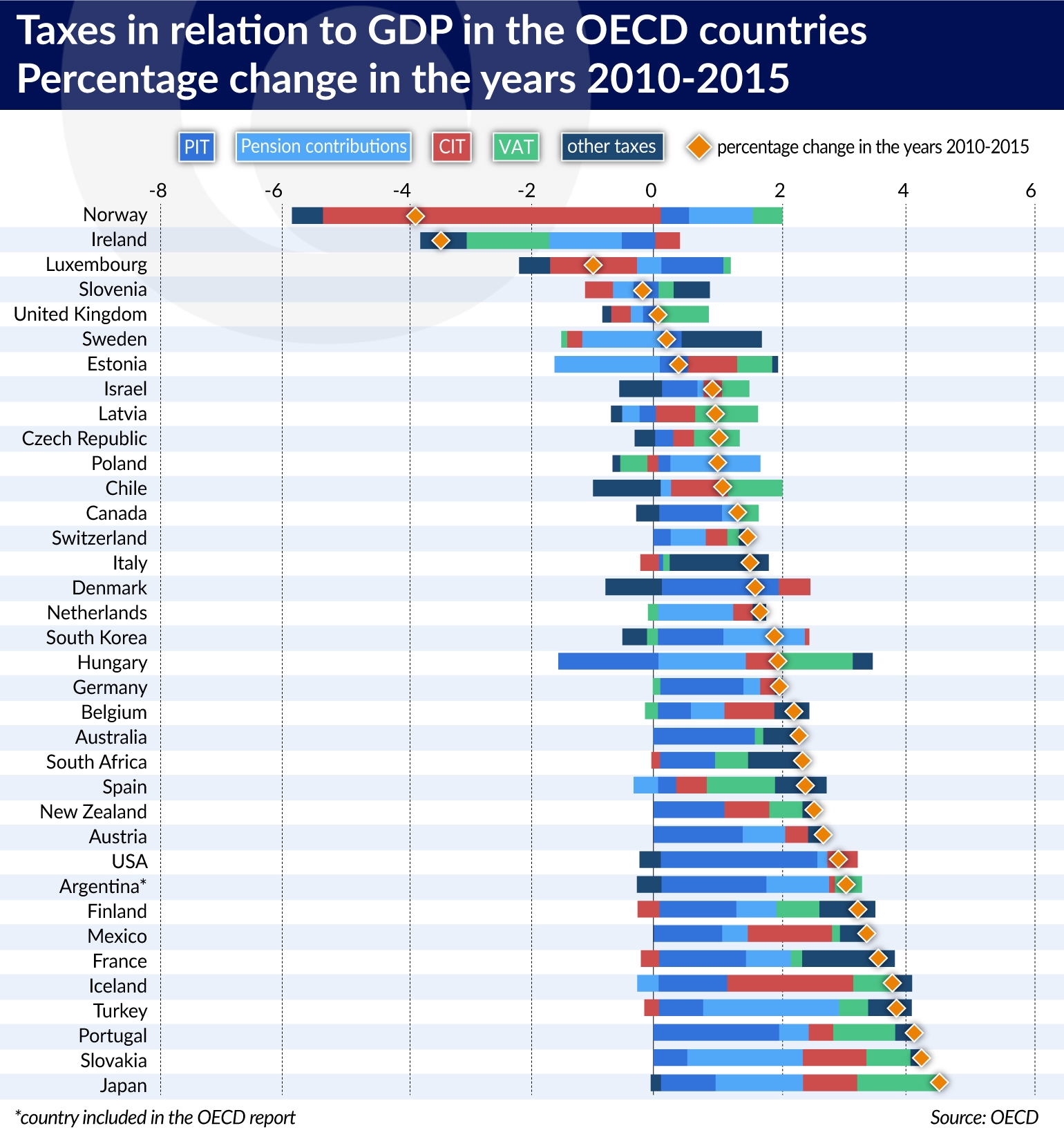

According to the recently published report – Tax policy reforms 2017 – the size of the tax burden in 32 countries covered by the OECD survey was 34.3 per cent in 2015, which is 0.1 per cent more than in 2014, and nearly 2 percentage points more than in 2009. In order to boost economic growth, governments are searching for opportunities to stimulate it, among others by reducing the tax burden. Many countries belonging to the OECD have already launched – and further countries have announced launching – changes in the tax systems aimed at encouraging greater economic activity.

The changes are not dramatic, as the budgetary capabilities have not yet improved significantly. Instead they mostly rely on a selective reduction of income taxes, along with a simultaneous stabilization and even increase of consumption taxes. The rate of corporate taxation (such as CIT) is falling, but is also made dependent on the fulfillment of conditions that are supposed to help in the development of the domestic economy. This is how we could interpret, for example, the announcement of the American administration that it would lower income taxes for companies that decide to repatriate their business activity to the USA. In some OECD countries, including Poland, efforts have been made to eliminate loopholes in the tax systems and to reduce tax fraud, especially concerning VAT.

Between Denmark and Mexico

The OECD report summarizes the tax changes introduced or announced in the member states in 2016. The implementation is often spread out over time. The goal of the changes is to lower the taxes being paid (except for Greece, which cannot afford it), with particular emphasis put on income taxes. These changes lead to declines in tax revenues, which in some countries are compensated with increases in consumption taxes or other charges, e.g. associated with the use of the environment.

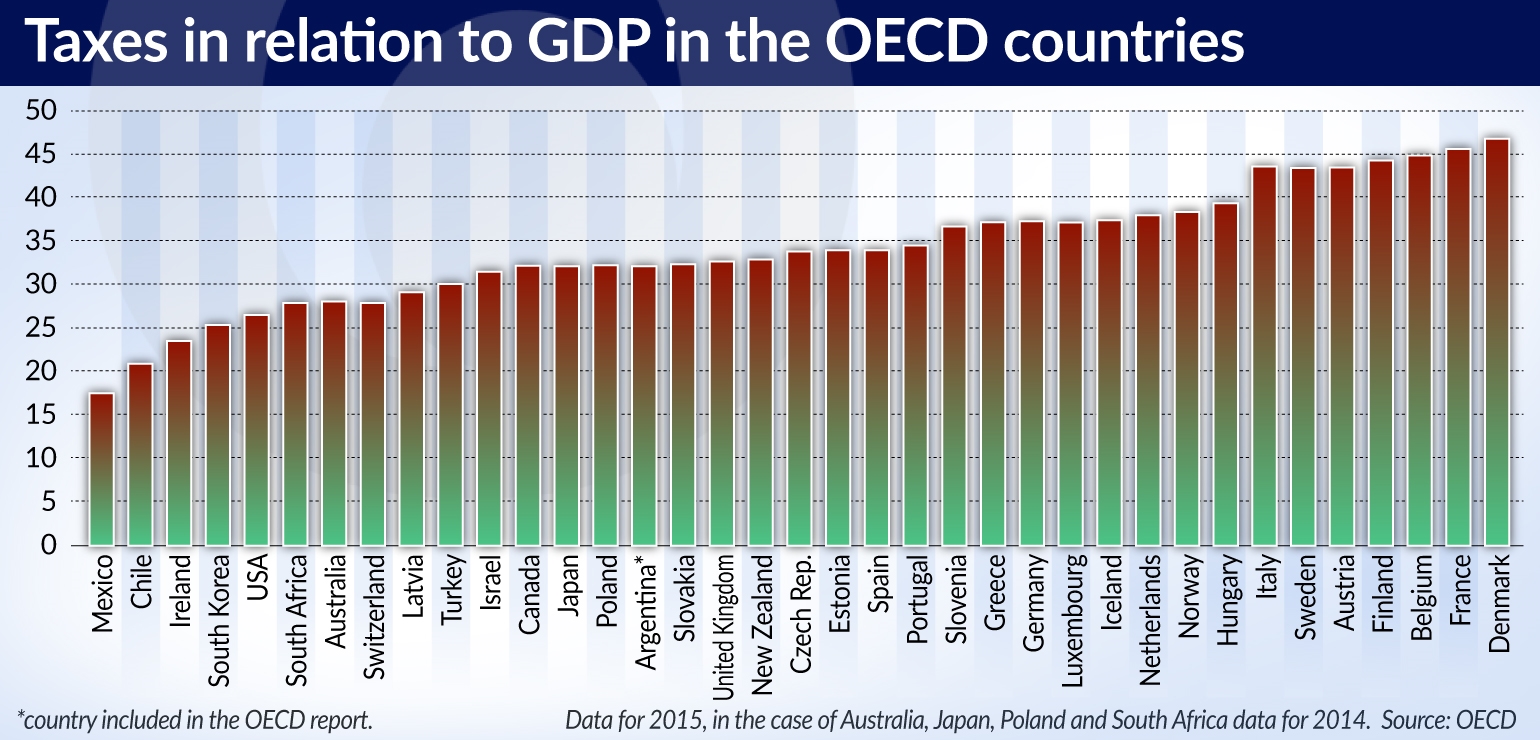

It’s difficult to find a common right way ahead. Among the OECD countries, on the one hand there are countries such as Denmark, where in 2015 the total tax burden has reached 46.6 per cent of the GDP (in France – 45.5 per cent, in Belgium – 44.8 per cent), and on the hand other – Mexico with a tax burden at a mere 17.4 per cent, or Chile at 20.7 per cent. Low tax burdens are also seen in Ireland and South Korea. The OECD report does not include the 2015 data for Poland, but in this respect the country ranks below the average for OECD countries, at a level close to Slovakia, Japan and Canada.

Ready for lower tax revenues

The most extensive changes in the tax systems are currently being implemented in several European countries, mainly member states of the European Union – Austria, Belgium, Greece, the Netherlands, Luxembourg and Hungary, as well as Norway. Except for Greece, they are all oriented towards fiscal stimulation, the aim of which is to accelerate economic growth. In 2016 the taxation of work was lowered in Austria, Belgium and the Netherlands. In 2016 and 2017 Norway introduced changes in the taxation of companies that have reduced the burden on companies, at the same time broadening the tax base. Tax changes beneficial to companies and the investment climate have been introduced in Hungary and Luxembourg.

The scale of reform is reflected in the size of the fiscal stimulus expected in these countries, calculated as the shortfall in direct tax revenues. In Austria the authors of the reform assumed the shortfall of approx. EUR2bn in 2016 and 2017, in Belgium – approx. EUR2.4bn in 2016, in the Netherlands – more than EUR4bn in 2016, in Hungary – approx. EUR1.7bn in 2017, in Luxembourg – EUR373m and in Norway – a total of EUR775m in 2016 and 2017. However, these countries are certainly hoping to achieve similar effects to those recorded in Ireland, where the recent reduction in the corporate income tax (CIT) has brought a big increase in economic activity and, consequently, an increase in tax revenues.

Less from the poor and more from rich

It is interesting to observe the trends currently unfolding in OECD countries in terms of taxation within individual categories of taxes. The taxation of income from work (PIT), and the social security contributions (SSC) are key components in the structure of the tax revenues collected in OECD countries. Together they bring in more than half of the total tax revenues – the PIT provides 24 per cent, and the SSC are responsible for 26.2 per cent.

However, there are major differences between individual countries. In Austria, Germany, Sweden and the United States the share of PIT, SSC and other income taxes even exceeds 60 per cent of total tax revenues. Chile, where this share is only 14 per cent, is at the opposite extreme. But this is an exception. In the case of New Zealand, Mexico and Israel – which are more representative – the share of the tax burden relating to work reaches approx. 40 per cent.

Regardless of the budgetary significance of work-related taxation, most of changes in taxation rules focus on the individual income taxes and payroll charges. The goal is generally to relieve taxpayers on the lowest and average incomes. In 2016, eight OECD member countries implemented non-marginal PIT rate reductions, and this year they have been reduced in 11 countries.

For example, Belgium abolished the 30 per cent PIT rate, by integrating the taxpayers covered by that tax rate bracket into the 25 per cent tax rate bracket. In Ireland, the Universal Social Charge contributions were decreased in 2015 and 2016. In Canada, Luxembourg and Slovenia, tax rate cuts were specifically targeted at middle-income earners. Slovenia, for instance, introduced a new tax bracket with a rate of 34 per cent and lowered the PIT rate of the highest bracket from 41 per cent to 39 per cent.

In some countries, such as Austria, the reduction of PIT rates for taxpayers earning lower and medium incomes is accompanied by increases for those with the highest earnings. In Austria, the existing system with three tax brackets has been replaced by a system with six tax brackets, along with a new top PIT rate of 55 per cent. In Canada, the tax rate on incomes between CAD 45 000 and 90 000 was lowered from 22 per cent to 20.5 per cent, and a new tax rate of 33 per cent was created for incomes over CAD200,000. The lower PIT rates were also reduced in Luxembourg, while the tax rate on the highest income was increased to 42 per cent. Similar adjustments were also introduced in Israel. In Finland, on the other hand, all tax rates were lowered uniformly as part of the stimulus package.

Changes in the PIT do not apply to the tax rates alone, but also concern the so-called tax base, changing the situation of different groups of taxpayers. The goal is generally to improve the situation of families with children at the expense of families that do not (yet or no longer) have dependent children. This is supposed to help – we are familiar with this issue in our country – in reversing the unfavorable demographic trends that affect almost all European countries.

In many countries another motivation for the currently introduced or planned changes in the PIT is to provide incentives for entrepreneurship and innovation. For example, Finland has introduced a 5 per cent reduction in income tax for entrepreneurs and self-employed persons. A new solution has been applied by Portugal, which reimburses one quarter of the expense on individual investments in start-ups. Tax facilities for beginning entrepreneurs have also been introduced in Italy. Similar changes have also been adopted in Australia, Canada, Estonia and the United Kingdom. Their goal is to generally lower the paid taxes while simultaneously expanding the tax base.

Contributions dependent on activity

As in the case of the PIT, the objective of changes in social security contributions (SSC) is typically to stimulate employment growth and competition. In 2016 the contributions paid by employers were reduced among others, in Belgium, Estonia, Iceland, Luxembourg and Switzerland. Italy introduced a two-year allowance for employers for each new worker employed on a permanent contract. In these countries, as well as Slovakia, lower contributions are also paid by employees and self-employed persons.

This is not a universal trend, however, as the SSC were in the same time raised in Spain, Greece and in Japan. The contributions will be increased, among others, in Finland, Germany and the United Kingdom. The direction of changes – it seems – depends not only on the need to stimulate the current or future economic activity, but also on the demographic situation and the labor market situation in the individual countries.

Marginalization of the CIT

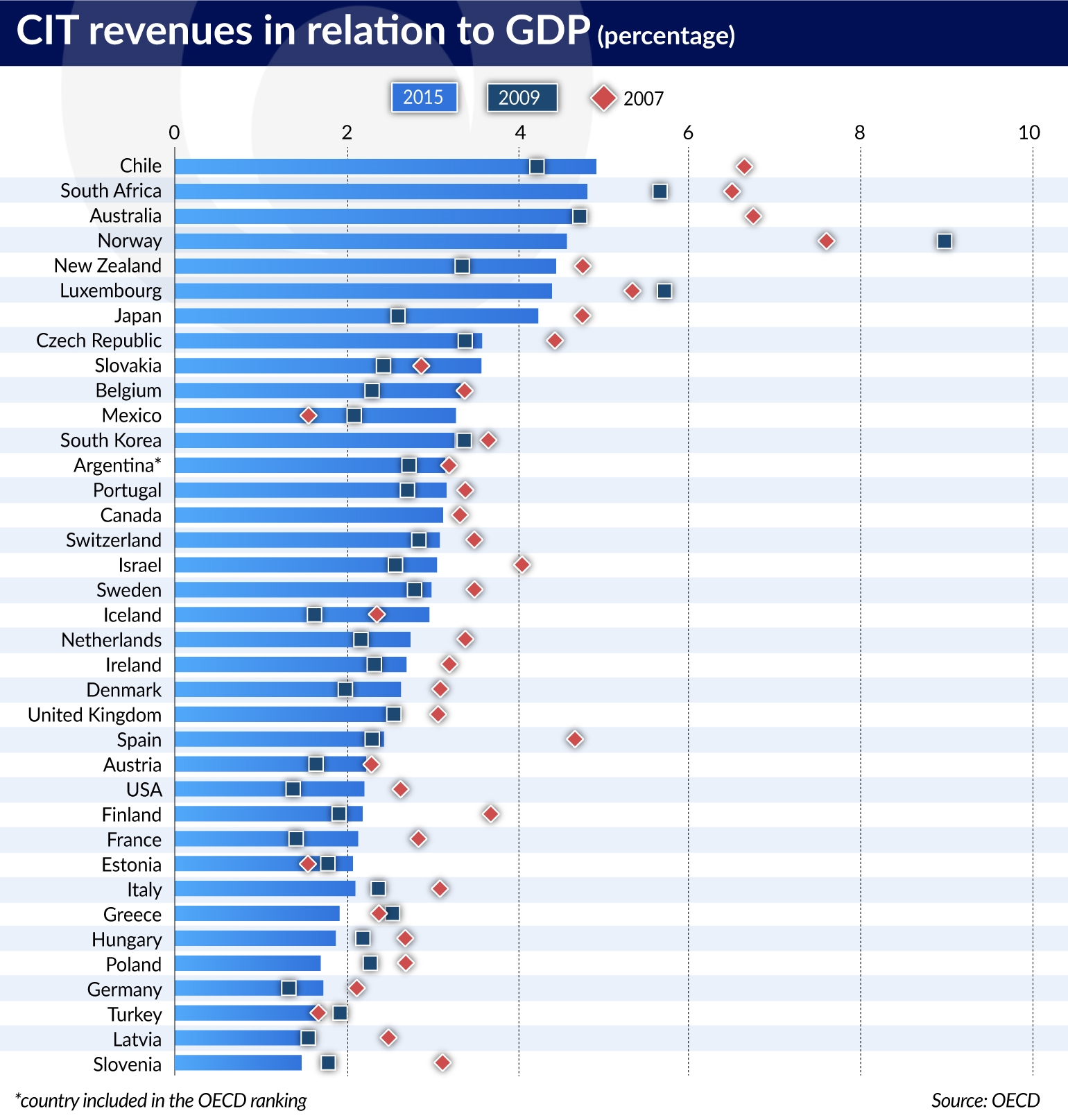

In countries belonging to the OECD the taxation of corporate income (CIT) has definitely less importance than the PIT and social security contributions. The CIT only provides 8.8 per cent of total tax revenues. Like in the case of other taxes, there are big differences in the importance of CIT revenues for the budgets of the individual countries. This tax has the least importance for the budget of Slovenia, where it only provides 4.0 per cent of the total tax revenues, and is the most important in the case of Chile (23.7 per cent).

A reduction of CIT is currently the most popular choice in the selection of fiscal tools aimed at stimulating economic development. In 2015 the corporate income tax was reduced in Estonia, and in 2016 similar tax changes were introduced in Japan, Spain, Norway and Israel. The reduction of CIT rates is also increasingly accompanied by exemptions or tax breaks for selected groups of companies (especially small and medium-sized enterprises) or associated with the types of enterprise expenditures preferred in the national economic policies (e.g. for research and development).

The OECD report on trends in taxation indicates that the tendency for a reduced role of CIT will continue in the coming years. Eight countries reduced CIT rates in 2017, and three more will do that in the near future. For example, Spain lowered the CIT rate from 30 to 25 per cent in 2016, Norway from 25 to 24 per cent in 2017, and Israel has been gradually phasing down the CIT rate from 26.5 per cent in 2015 to 23 per cent in 2018. Against the background of these countries CIT is still relatively low in Poland (19 per cent), but since this tax is often being used against other countries in international competition, Poland’s advantage in this area is shrinking. It’s worth paying attention to the radical move made by Hungary, which reduced the CIT rate to just 9 per cent this year. The reduction of the CIT rate to 15 per cent would certainly improve the situation of small companies in Poland.

The downside of the increasingly common use of CIT as a tool of economic rather than fiscal policy, is the growing complexity of the corporate tax system and the multitude of principles for tax relief and exemptions applied. This encourages companies and countries to use tax arbitrage in investing and transferring profits. Unfair competition in this field is supposed to be counteracted by a package of recommendations and standards concerning CIT (BEPS – Base Erosion Profit Shifting) developed in 2015 among the 20 largest economies in the world (G20). Thus far, however, the effectiveness of actions taken at the international level seems to be fairly limited.

Lower revenues are compensated by the taxation of consumption

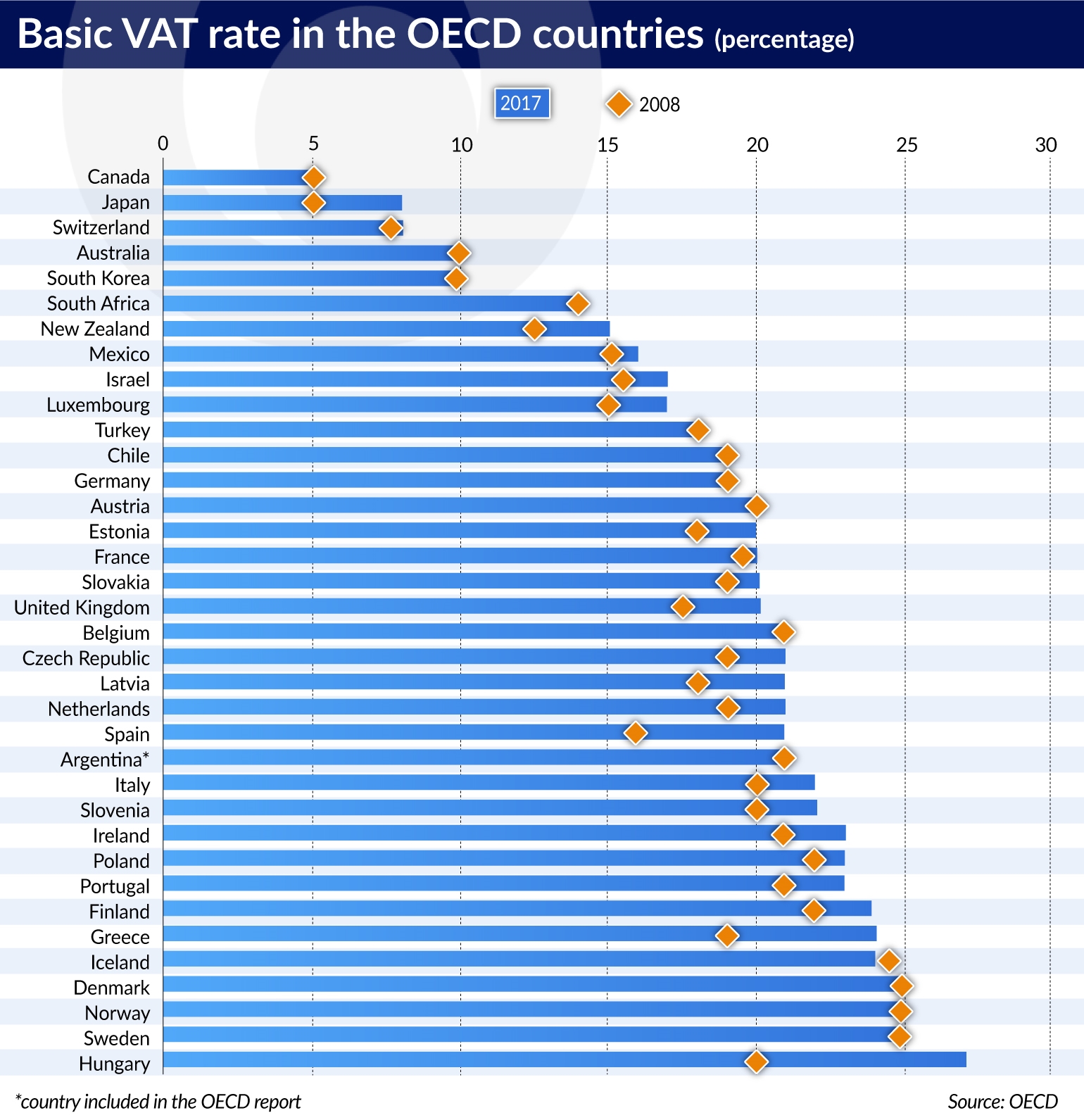

Countries generally try to compensate for the budget shortfalls associated with reduced rates or the introduction of various preferences in the PIT or SSC system with a rise in revenues from consumption taxes, especially the VAT. The focus on VAT mainly arises from the importance of this tax in the budgets of most OECD countries (it provides an average of 19.2 per cent of tax revenues), with the noted exception of the USA, which has no at all, and whose budget revenues are mainly provided by the income taxes.

The potential changes in the VAT will most likely not include changes in the basic rates, which are already quite high in the OECD countries, but will involve the limitation of areas where preferential rates are applied. In recent times, only Greece raised its basic VAT rate in 2016 (from 23 per cent to 24 per cent) for obvious budgetary reasons. The VAT rates were also raised by some provinces in Canada. Meanwhile, Italy withdrew from the plans to raise the VAT rate from 22 per cent to 24 per cent. However it left open the possibility of reversing this decision and raising the VAT rate to 25.9 per cent in 2019.

The fiscal authorities are showing a much greater interest in the preferential rates. For example, in 2016 Norway raised the preferential VAT rate applicable to passenger transport, accommodation and movie tickets from 8 per cent to 10 per cent. At the same time Austria raised the preferential VAT rate for hotel accommodation, tickets for cultural events and for domestic air travel from 10 per cent to 13 per cent. Greece abolished the VAT preferences enjoyed by the Greek islands.

However, the fiscal goals are intertwined with the objectives of economic stimulation also in the case of VAT. Some OECD countries extend the application of preferential tax rates – where allowed by the budgetary situation – in order to encourage certain types of consumption and production or services.

In 2016 Slovakia and Turkey reduced the VAT rates for certain food products. In 2017 similar changes were adopted by Hungary and Portugal. Hungary has also reduced the VAT rate on newly-built homes and restaurant services. Sweden introduced a reduced VAT rate for minor services such as the services bicycle or and shoemaker’s workshops. The Czech Republic provided support to publishing houses by reducing the VAT on the sale of newspapers from 15 per cent to 10 per cent. Meanwhile Switzerland and Norway introduced a lower VAT on on-line sales of newspapers.

The preferential treatment of selected types of production or services is accompanied by a marked tightening of policies pursued by the fiscal authorities in many OECD countries with regard to fraud in this area. The OECD report points out the broad package of anti-corruption solutions which have been applied in Poland since the beginning of 2017 as one of the positive examples. Austria, the Czech Republic and Slovakia also started fighting VAT-related fraud in 2016.

New trends

The economic recovery along with the simultaneous stabilization of public finances encourages many countries to find ways of accelerating economic growth. This purpose is served, among others, by new fiscal incentives. Their application is becoming increasingly individualized, however, and it is tailored to the specific categories of income, activity and groups of taxpayers. In this sense, taxes are becoming an instrument of not only fiscal but also economic policy.

The more general directions for further changes in taxation are also taking shape. This applies, for example, to sales and consumption. The VAT will increasingly also cover the digital economy – the spontaneously growing online sales and online provision of services. Another expected direction is the taxation of products whose consumption is considered harmful. In addition to cigarettes this category is being extended to certain beverages, especially sugary drinks. Finally, we should expect an increase in fees for environmental damage.