Tydzień w gospodarce

Category: RaportyPrzegląd wydarzeń gospodarczych ubiegłego tygodnia (25–29.04.2022) – źródło: dignitynews.eu

In neoclassical economics it is assumed that capital flows from wealthy countries to poor countries. On the global scale, developed nations should ultimately be the net exporters, while developing countries should be the net importers of capital. The conclusions derived from the theory in relation to the overall foreign investments are not confirmed by empirical data, as shown in a study conducted by the American economist Robert Lucas in 1990.

However, in the case of foreign direct investment (FDI), the analysis of the data suggests, that the developed countries are the largest investors in the world, while the developing countries are the recipients of half of global FDI. These data, however, are distorted, as some of the OECD member states (mainly Luxembourg and the Netherlands) serve the role of intermediaries in investment transactions, and for that reason alone are among the biggest recipients of investments in the world.

The conclusions resulting from the macroeconomic concepts relating to FDI, and in particular J.H. Dunning’s concept of the so-called investment development paths, as well as Terutomo Ozawa’s dynamic theory of economic development and competitive advantage (1992), also indicate, that as a given country becomes wealthier it should change its status on the world’s investment map and move towards becoming a net exporter of capital.

On the one hand, the previous development of foreign direct investment in Poland reflects the global trends. On the other hand, these tendencies can be explained by factors resulting from the life-cycle of investments (the data on FDI are presented in accordance with the current benchmark standard for direct investments defined by OECD in 2008, and leave out transactions of so-called Special Purpose Vehicles (SPV) registered in Poland, which have no impact on the Polish economy).

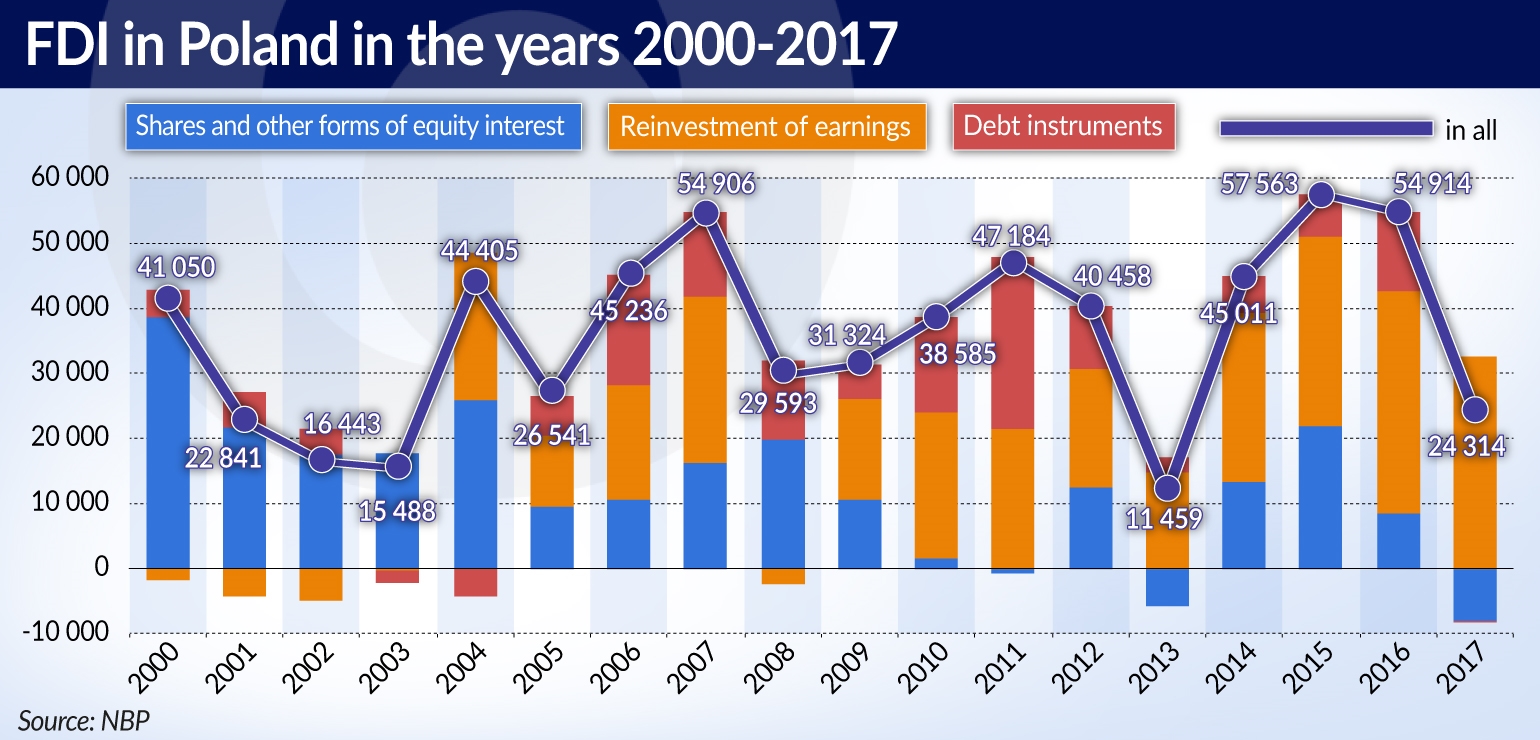

We can distinguish three phases in the history of FDI inflows to Poland. The first phase began with the entry of new investors in the early 1990s and the privatization of the state-owned enterprises. The volume of the inflows increased along with the liberalization of capital flows following Poland’s accession to the OECD. In this phase, capital primarily flowed in through the acquisitions of capital shares (equity interests) in existing companies and their subsequent recapitalization. At that time the profits of companies with foreign capital were relatively small, and the reinvested earnings were often negative. This was mainly due to the fact, that many investments were still at their initial stages of development, but also due to the relatively high rates of the corporate income tax.

Starting from the beginning of 2004, the CIT in Poland was reduced from 27 to 19 per cent, and from that point on, companies with foreign capital started reporting and reinvesting profits. This moment can be seen as the beginning of the second phase in the inflow of direct investments. During that time, the role of financing with debt instruments and reinvested profits increased, while the inflow of capital in the form of equity interest was decreasing. The inflow of capital broke down twice, in the years 2008-2009 and in 2013, which was the result of turmoil in the global financial markets.

The rebound after 2013 marked the beginning of the third phase in the inflow of foreign direct investment. It is characterized by a dominant role of reinvested profits, while the balance of transactions on capital shares and debt instruments can also be negative at times, when foreign investors decide to exit from their investments in Poland. The high volumes of reinvested profits largely result from the fact, that the previously implemented investments have entered into the phase in which they generate revenues. Similar characteristics of the transition through the various types of investments are also observed in the other countries of the region. In 2015, Filip Novotny described the characteristics of this phenomenon for the Czech Republic.

In the 1990s and in the early 2000s, as a result of the above-mentioned entry of international corporations into Poland, the value of FDI grew significantly, reaching the record level of 5 per cent of the national GDP in 2000. Since that point, a decrease in the inflow of FDI can be observed. Prior to the outbreak of the global financial crisis, that is, in the years 2004-2007, the average inflow of FDI to Poland amounted to 4 per cent of the GDP. In the subsequent years, the value of FDI declined even further, reaching the level of 2 per cent of the GDP. So what is the reason of this decline?

Firstly, this is the result of a general decline in the inflow of foreign capital to emerging economies after 2010, which has been pointed out by the IMF in one of its World Economic Outlook reports.

Secondly, the reduction in volume of FDI is linked to the life-cycle of investments. In the initial periods, the investment must be financed with external capital, which is associated with a relatively large inflow of funds from abroad to a given country. This capital may come from abroad or may be guaranteed by a foreign investor. Thus far, however, financing mainly came from abroad due to the lower cost of capital in foreign countries. Only once a given business activity develops thanks to this capital, it is possible to reinvest the profits from such an investment. At that point, however, the inflow of new funds from abroad is reduced, because the investment is financed from the current revenues. This causes the value of foreign direct investment to decrease.

Thirdly, the lower value of FDI in Poland is linked to a change in the sectoral structure of the inflowing long-term capital. An increasing number of new investments are located in the services, in particular in the so-called modern business services (such as IT, outsourcing, financial services, accounting, legal services, etc.). Such investments are in general less capital intensive than investments in manufacturing.

The launch of an investment project in the services sector generally involves renting out office space and purchasing or leasing equipment necessary for the provision of services (telephones, computers, etc.), outsourcing of certain business processes (e.g. recruitment). Such an investment does not require significant capital expenditures, and its current operations can be financed from the generated revenues. Meanwhile, an investment in manufactuirng requires finding a suitable plot of land, building a factory and equipping it with machines.

It’s worth noting that the inflow of foreign capital into the services is associated with the establishment of service centers by international corporations. These centers are intended both for the internal use of the corporations and for the provision of services to external clients. The high qualifications of employees and the relatively low labor costs in Poland in comparison with the other Central and Southeast European (CSE) countries are conducive to such investments. The number of foreign-owned shared service centers in Poland is growing rapidly. According to data from the Association of Business Service Leaders, in the Q1’18, there were 839 such centers operating in Poland, compared with 459 centers at the beginning of 2013. ABSL predicts, that in 2019 their number will grow to 900. One of the consequences of the increasing inflow of foreign direct investments into the sector of services, which are usually more labor-intensive than investments in industry, is the dynamic growth in the number of new jobs in Poland. The data presented by ABSL indicate, that in the Q1’18 shared service centers established by foreign companies employed 225,000 people, while at the beginning of 2013 they employed fewer than 100,000 people. The ABSL’s latest projection indicates, that in 2019 the number of jobs in the sector of modern business services will increase to 250,000.

The authors are employees of Poland’s central bank, NBP. The article presents their private views, and is not an expression of NBP’s official position.