Tydzień w gospodarce

Category: Trendy gospodarczePrzegląd wydarzeń gospodarczych ubiegłego tygodnia (30.05–03.06.2022) – źródło: dignitynews.eu

Lately, hardly a day passes by without new alarming information about the effects of rapidly progressing climate change. For example, global warming is leading to excessive jellyfish and squid populations and is causing extreme weather conditions and natural disasters that harm the economies and reduce agricultural production, thereby deepening social inequality. While the rise in global squid population is not likely to prompt decision makers towards action, growing financial risks and concrete economic losses are forcing them to take specific decisions relating to policy and investment. This is because climate change is currently one of the main threats to the long-term stability of the global economy.

According to the report published in June 2019 by the international organization CDP (formerly known as the Carbon Disclosure Project), more than 200 of the world’s largest companies, including Apple, JPMorgan Chase, Nestlé, and 3M, see climate change as a threat to their business. The companies themselves have estimated that the problems related to climate change, such as disruptions in supply chains, the problems of debtors (e.g. farmers whose crops will be affected by droughts) with the repayment of their liabilities, rising energy prices, and the need to adapt to new regulations, could generate total costs of USD1 trillion over the next five years. According to the estimates of the Climate Bonds Initiative, the financing of „green” investments should reach exactly that amount by the end of 2020. Moreover, it should be growing with each year in order to recapitalize the sectors of renewable energy, energy-efficient construction, the circular economy (including waste management and water management) as well as ecological transport, and to enable the use of agricultural land in a manner compatible with sustainable development.

The push for the development of green financing is the result of the staggering costs already borne by the economies due to global warming. In the 2015 Economist Intelligence Unit report, the value of assets at risk whose valuation depends on climate change was estimated to reach between USD4.3 trillion and USD43 trillion by the end of the century. Floods or the lack of permanent access to water caused by climate change are already contributing to conflict-inducing migrations. According to predictions of the World Bank, the problem of water scarcity, which is exacerbated by global warming, could cost some regions of the world (including Poland) up to 6 per cent of their GDP. In turn, according to the European Commission, „the increase in weather-related natural disasters means that insurance companies need to prepare for higher costs”, while, „banks will also be exposed to greater losses due to the lower profitability of companies most exposed to climate change or highly dependent on dwindling natural resources.”

The disclosure of the scale of these threats was the direct reason why almost 200 countries signed the Paris Agreement in 2015. The document sets out a global action plan which is supposed to protect humanity from the threat of far-reaching climate change by limiting the global temperature rise in this century to well below 2°C above pre-industrial levels. The conclusion of the agreement also initiated a detailed review of the global financial system by the UN, the G20 and the European Commission. The goal of these activities is to create a framework for the financing of investments enabling the implementation of the Paris Agreement.

Already in 2015, the Financial Stability Board (an international body acting on the basis of a mandate provided by the G20) initiated the creation of the Task Force on Climate-related Financial Disclosures (TCFD) led by Michael R. Bloomberg. The recommendations prepared by that group were one of the reasons why in 2017 the European Commission implemented a directive pursuant to which listed companies, banks and investment funds employing over 500 people and with a balance sheet total of over EUR20m or with net turnover above EUR40m, are required to report so-called non-financial data.

Besides reports, necessary to assess the risk associated with climate change, the most urgent issue relates to the sources from which the mitigation of these risks is to be financed. Research based on computer modelling, commissioned by the Intergovernmental Panel on Climate Change (IPCC), has shown that the risks associated with global warming could soon cost the global financial sector between USD1.7 trillion and USD24.2 trillion if appropriate, preventive measures are not taken. The authors of the report entitled “The climate finance domino, Transition risks for the Polish financial sector”, prepared in 2018 by the WiseEurope organization, emphasize that due to the fact that low-emission technologies are highly capital-intensive, implementation of the changes resulting from the provisions of the Paris Agreement will require substantial investment expenditure. According to a report of the TCFD, on a global scale these activities will translate into additional investments of USD1 trillion annually. Meanwhile, it is estimated that global annual expenditure on green infrastructure of USD6.9 trillion per year is required in the period until 2030. In the case of the EU, the investment gap will amount to EUR180bn annually until 2030. Mobilizing these additional funds is a huge challenge both for national and local authorities.

So far, financial markets have been more likely to finance mines than, for example, renewable energy sources, even though they officially supported green investments in their policy. The UN Green Climate Fund created after the Paris Summit, which was supposed to be supported by the member countries of the United Nations, failed to collect the required amount of USD100bn for projects implemented in developing countries. In recent years it has only managed to distribute USD5bn for about 100 projects in the form of loans, grants and loan guarantees. Only this year, the six largest multilateral development banks increased the financing of projects aimed at reducing emission intensity and addressing climate risks by 22 per cent — up to the amount of USD43.1bn in 2018. In the case of the European Bank for Reconstruction and Development, green financing is supposed to account for 40 per cent of all projects next year.

Meanwhile, developed countries are increasingly turning to special bonds in order to finance their own infrastructure protecting against climate change. The estimated amount necessary to save the world (and the individual economies) currently only accounts for 1 per cent of the entire global bond market, worth about USD100 trillion. Until recently, no one knew about bonds used to finance green (i.e. environmentally friendly) investments. Over the last decade the global cumulative issuance of green bonds has risen from zero to USD521bn. The issuance of green bonds amounted to USD179bn in 2018 alone, and is expected to reach USD200bn in 2019. The development of this market will certainly be promoted by the recent decision of the Norwegian parliament. In June 2019, the local legislature made a decision which formally obliged Norway’s Oil Fund to divest from 150 companies in the oil and gas industry, as well as large mining companies and to redirect USD20bn (2 per cent of the fund’s assets) to investments in renewable energy, starting with wind and solar projects on developed markets.

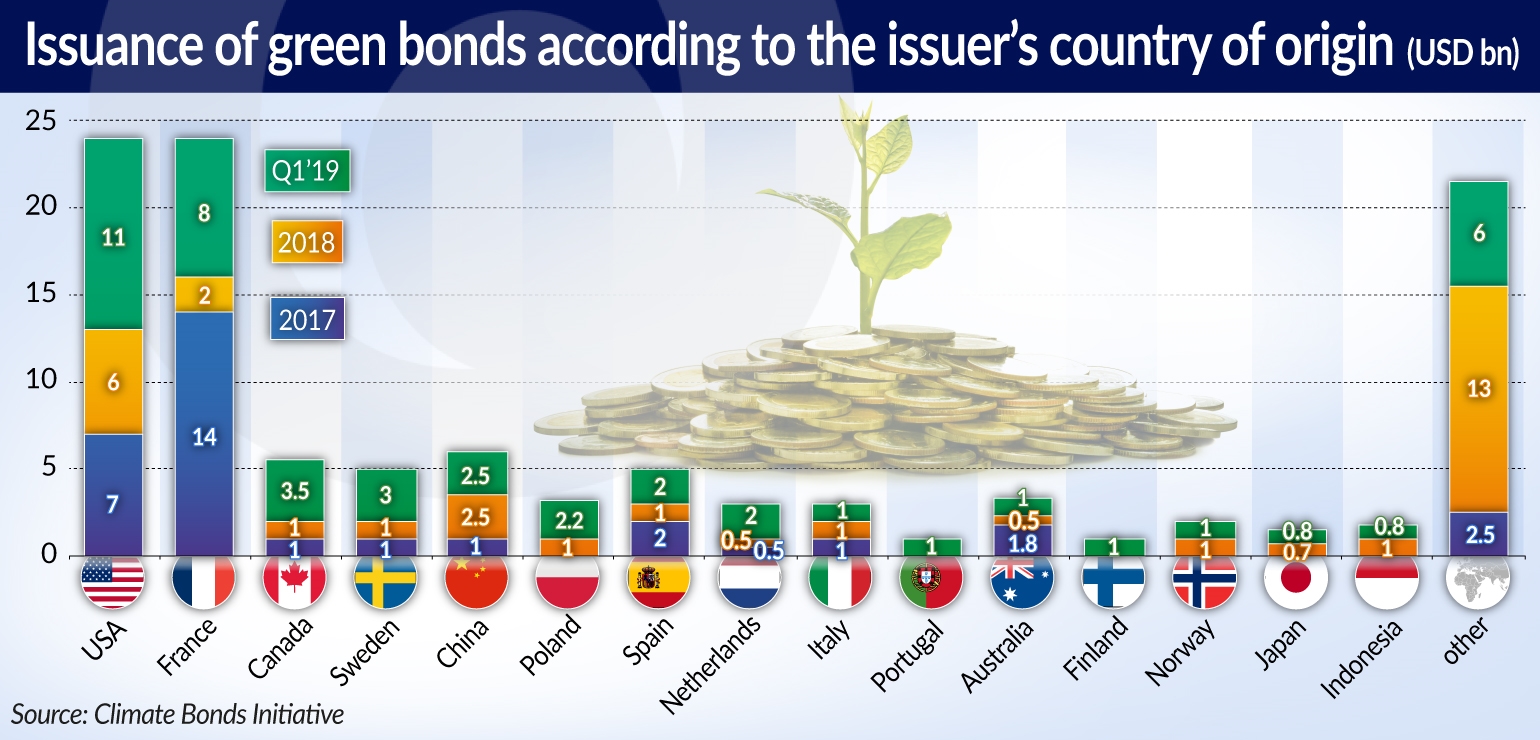

Green bonds started to become popular on the capital markets in 2013. They are distinguished by the specific goal for which the funds obtained from the issue must be allocated. They are used to finance or refinance projects related to environmental protection in the broad sense (e.g. renewable energy, energy efficiency, water and wastewater management, and waste management). When it comes to government bonds, France is currently issuing the most green bonds. However, Poland was a pioneer in green bonds at the national level. In December 2016, as the first country in the world, Poland issued 5-year green bonds with a nominal value of EUR750m. They were mainly purchased by investors from Germany, Austria, the Benelux countries, the United Kingdom and Ireland. Some of the obtained funds were to be used for tax breaks and subsidies for companies producing green energy, and for prosumers returning energy to the system as part of a discount scheme. In 2018, Poland issued more green bonds with a nominal value of EUR1bn.

The issue of green bonds may be carried out not only by states, but also by companies (e.g. from the energy or public utilities sector) or by local government units. Interestingly enough, the biggest issuers are mainly enterprises from countries considered to be the biggest polluters — the United States (20 per cent of the issuance value in 2018) and China (18 per cent). However, these countries are the seats of companies, such as the internet giants, which need investments in order to reduce the costs associated with the energy necessary to cool their servers. Moreover, their operations are increasingly frequently directly threatened by the effects of extreme weather conditions: floods, hurricanes, etc. Among the countries, the biggest issuers include France (6 per cent), Germany (5 per cent) and the Netherlands (4 per cent).

Local government units, especially in Europe, are also issuing their own bonds for green investments. They also allow their residents to decide the allocation of the funds obtained in this way. Lisbon was the first city in the world to introduce a „green” participatory budget. At the same time, it became the first local government unit that has benefited from the City Finance Lab platform created by the European Institute of Innovation and Technology. This platform is supposed to support European cities in the implementation of low-carbon solutions consistent with sustainable development. For this purpose it will act as an intermediary between local government units, scientific institutions, enterprises, and financial institutions in the implementation of solutions proposed by the local community.