Tydzień w gospodarce

Category: RaportyPrzegląd wydarzeń gospodarczych ubiegłego tygodnia (16–20.05.2022) – źródło: dignitynews.eu

Warsaw Stock Exchange (Penn State University Libraries, CC BY-NC)

The move is prompted by a change of the conditions that had helped turn the WSE into the region’s largest bourse.

(Infographics: Darek Gąszczyk)

The structural factors that made the exchange grow faster than the Polish economy for many years disappeared at almost the same time as a slump in the global economy. The first factor was privatization of state controlled companies, providing a steady supply of new listings. However, in recent years the number of privatizations has dwindled.

The second was open pension funds, which – cash-rich thanks to social insurance contributions – helped support a continued demand for shares. But the funds are only a shadow of themselves after reforms two years ago. Now they are mostly sellers and not buyers of shares.

Those changes happened as China’s economy slowed and investors began pulling out of emerging markets. “We see that the Stock Exchange is putting a great deal of effort into attracting liquidity. Players want to trade large volumes, but capital is flowing out at the moment. We also face a political risk,” said Łukasz Boroń of Erste Securities at the Futures and Options World Conference.

Another challenge for the Warsaw Stock Exchange is the Capital Markets Union, a project announced by the European Commission. Its aim is to raise capital to finance the non-banking sector, in other words capital markets. The WSE sees more risks than opportunities in connection with CMU, which was presented on September 30, 2015.

The main risk is that foreign investors will flee to Europe’s largest markets like Frankfurt and above all to London. If that happens, regional stock exchanges could be hurt. Those fears are not unfounded.

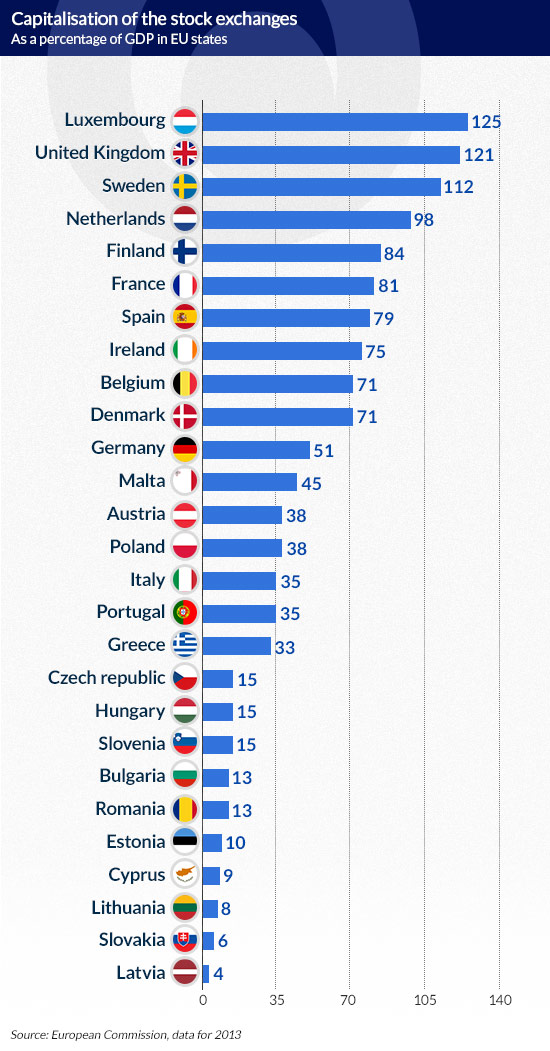

Since the crisis, the capitalization of almost all European stock exchanges has declined, but until recently, stock price indices in some markets soared. While in 2007 the capitalization of EU stock exchanges accounted for 85 per cent of the EU’s aggregate GDP, in 2013 it was only 64.5 per cent, according to the European Commission. Capitalization of the Warsaw Stock Exchange reached 38 per cent of Poland’s GDP in 2013. This is similar to Austria, and slightly higher than in Italy or Portugal, but still well below the EU average and also below the share of banking sector assets in Poland’s GDP.

(infographics Dariusz Gąszczyk)

In this situation, the WSE updated its strategy in 2014. It wants to dominate the region and gain a leading position in trading shares, as well as build a strong regional position in commodities and derivatives thanks to the Energy Commodities Market and the Financial Instruments Market.

The WSE is focusing on the derivatives market at a time when both brokers and investors are facing new regulatory challenges. Future Commission Merchants (FCMs) – the only brokers who can have direct access to the market – must meet capital requirements. For example, they have to pay traders in such a way that bonuses do not exceed their basic salary. This could mean a sharp increase in basic salaries. In the derivatives market this is further compounded by collateralized debt obligations (CDO).

“We cannot provide all clients with everything. We need to segregate assets which we trade acting as brokers. The days when you could be a small player in many places are gone. You have to be a large player in one place. We are forced to select strategic partners,” said Matt Cullimore, executive director at Morgan Stanley.

Such an approach by the largest players does not bode well for their interest in new products on the Warsaw Stock Exchange. However, the single banking license, which comes into effect this year and gives banks direct access to the stock exchange, may help generate turnover. So far banks had access to the stock exchange only through brokerage houses, but these were financially too weak to buy assets on their own account. Opening access for banks may boost liquidity in bond and derivative markets.

“Banks are going to organize trading … It is extremely beneficial for our products, particularly bond and share futures,” said Grzegorz Zawada, the WSE’s deputy president.

In July, the Polish Financial Supervision Authority issued a recommendation to banks to settle their PLN interest rate products, in other words, IRS and FRA swaps, in the clearing house. At the moment, some participants are trying to meet these requirements, while others have failed to fully adjust. If, however, the idea of settlement of products from the interbank market catches on, it will need only one more step to put these contracts in the regulated market.

The Warsaw Stock Exchange scored a considerable success in May. The Commodity and Futures Trade Commission (CFTC) – the American authority overseeing derivative markets and participating institutions – certified futures contracts on the WIG20 index, which means that this instrument can be found in portfolios of US investors. Now, the WSE is seeking accreditation for index options with the American Securities and Exchange Commission (SEC).

“Now that the CFTC has certified our WIG20 futures contract, we will be able to attract American investors to our market,” said Zawada.

The WSE is counting on the TGE and hopes that with futures contracts for electricity, and in the future also for gas, the Warsaw bourse will become a regional power.

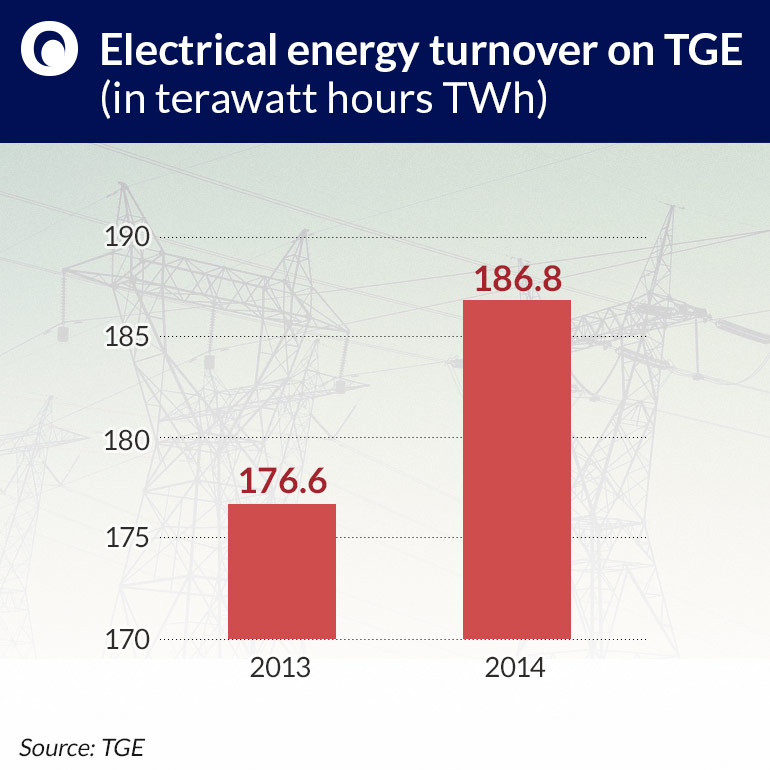

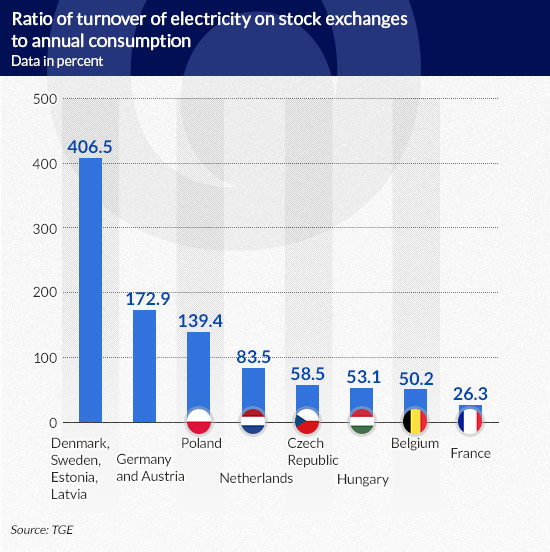

Electricity is the main commodity traded on the TGE. These are forward contracts with future delivery dates. In 2014 the total trading volume on markets of physical delivery of electricity amounted to 186.8 TWh, or 119.4 per cent of domestic energy production and 117.7 per cent of energy consumption. This is a 5.8 per cent rise on the previous year’s figure, reports TGE. Four years ago, trading volumes were less than half of this value. From the point of view of derivatives trading, large volumes and liquidity in the underlying market look promising. Other commodities traded on the TGE include natural gas and CO2 emission allowances.

Now the TGE is launching the Financial Instruments Market, with the TGe24 index for electricity contract futures as the first such instrument. This index is calculated once a day (at 10:30 a.m.) as the arithmetic mean of the prices in the previous hours. It has been calculated since June 30, 2015. The quotation will include two series of annual contracts for two consecutive years, as well as four series of quarterly contracts and four series of monthly contracts for the subsequent four months. The minimum trading unit will be 1 MW and the quotation step will be 1 gr / MW.

Trading will take place from Monday to Friday, and the underlying market for futures contracts will be the Day-Ahead Market for electricity.

Brokerage houses and, in the future, banks and foreign financial institutions, as well as energy companies operating on the physical supply market may have direct access to the market. The TGE is now holding talks with other infrastructure providers.

“We are trying to find out how many banks and brokerage houses in Poland will offer clearing and settlement of derivatives, who to cooperate with. I will be happy if this starts working in a 9 months’ time,” said Jarosław Ziębiec, coordinator of the Regulated TGE market.

According to TGE, trading on the Financial Instruments Market will be primarily performed by companies that, thanks to TGe24 index derivatives, will secure buying and selling prices of electricity for a longer period of time and will not have to take positions on the physical delivery market, as well as those that need to manage the risk of changes in energy prices.

Growth in commodity markets in the EU, and especially in energy commodity markets, should be driven by the European energy union project. The construction of interconnectors, including gas links, between national networks and free access to the network mean greater accessibility and greater liquidity of resources. It also increases their contracting possibilities.

“There are prospects of increased trading thanks to the energy union,” said Cees Vermaas of CME Group.

Transmission networks are already in place, however, there are problems. In northern Germany, the state-subsidized generation of electricity by wind farms has developed on a large scale. But this cheaper power not only distorts competition, but also causes network congestion and destabilization– among others in Poland and in the Czech Republic. As a result, Polish operators have tried to limit the delivery of Germany electricity to Polish networks.

Bundesnetzagentur, the German energy market regulator, announced in June that it is seriously considering the separation of the German and Austrian energy markets (linked since 2002 to prevent German electricity from flowing abroad). That would be a serious challenge to the energy union.

(infographics Dariusz Gąszczyk)

In the years after the crisis, new derivatives markets started to mushroom. Some quickly gained a very strong position like, for example, CME Europe, established last year, which trades 3 billion contracts a year with a value of one quadrillion (1024) dollars.

The emergence of new firms is accompanied by consolidation of the industry. In the 1970s in the United States there were 362 licensed FCM companies, of which only about 70 have survived until today, with just 52 providing services to customers.

“Business models have changed, and it is difficult to generate rates of return amidst low interest rates, especially in the extensive interest rate contracts market,” said Carl Gilmore, co-chairman of Wedbush Futures, a derivatives broker based in Chicago. “We had to redefine our business models and structures. We had to adapt ourselves in order to survive.”

Will traders and investors from abroad come to Warsaw in a situation of high competition in the derivatives market and constant struggle for liquidity? It all depends on whether and how quickly the Warsaw energy derivatives market manages to raise enough liquidity for large players.

“It will be extremely difficult for new markets to increase liquidity,” said Ian Firla, director of brokerage company OSTC Poland.

“Once we have high liquidity, we will not have to fear that the market will flee to London,” said Muammer Cakir, the head of the Istanbul derivatives stock exchange.

Entry into a new market means high costs for both brokers and derivative traders. Trading is undermined by market fragmentation. It is necessary to find a broker in each market, and that, in turn, means lower liquidity.

“I see an opportunity to develop futures products. With increasing price volatility, many companies want to hedge their positions. Yet for a company the creation of a trading floor means a high cost, as it needs to have access to each market separately,” said Sebastian Jablonski, a trader at Vattenfall.

“The start is the hardest. Low liquidity, lack of possibility to increase it, and the limited number of derivatives are the challenges faced. Whoever comes first is the first liquidity provider, and they need it themselves. Everyone waits for the market to open, yet nobody wants to be the first,” added Oskar Pecyna, member of the supervisory board of Polish brokerage firm Skyhedge.

Stock markets are in a similar situation, even the large ones, which is why they are making cooperation proposals to small partners.

“Regional markets have a good chance of success, but none of the local stock markets will gain a global position. Therefore, it is necessary for stock exchanges to cooperate,” said Vermaas.

The Warsaw Stock Exchange’s priority is organic growth. “I hope that domestic investors will provide liquidity. We want to pursue our own local strategy. We opt for organic growth and do not envisage any partnerships,” said Zawada.

The danger for smaller exchanges is that larger partners will maximize their own benefits, creating a one-sided relationship.

“Of course, we are taking into account partnership models, but the concept „99 per cent for us, 1 per cent for you” complicates matters,” said Tom O’Brien, international sales director at the Moscow Exchange.

TGE has a tough fight ahead to achieve critical mass. If it succeeds, the commodity derivatives market has good prospects. But if it doesn’t, then the WSE may have to think seriously about a strategic alliance.